Introduction

Over

long periods of time, the S&P 500 outperforms most financial assets; but

paradoxically, no one knows its proper price and therefore its projected rate

of return.

Existing economics either assumes that the

“equilibrium” quoted price is always right, and thus there are no markets; or

that its proper price in fluctuating markets is unfathomable.

With one minor change in assumption, our research

demonstrates it is possible to derive the proper price of the S&P 500, and

thus its prospective rate of return, in real financial markets.

Ronald Soong

Horizon Capital Research, Inc.

“Valuation (and therefore investment

rates of return) is the central concept of

finance. While investors believe that the process is difficult and

fraught

with errors and assumptions…valuation (ought to be) approached with

rigor

and care. Without methods to assess value, capital budgeting (investing)

becomes

impossible.”

A

Quote

Portfolio Returns in Real Financial

Markets

This

discussion is about real financial markets, not a market conforming to a

short-term theoretical statistical model nor to a state of equilibrium, with

lots of algebra, but no markets. This discussion is about real portfolios in

real markets, which offer people the opportunities to buy or sell according to

their needs.

Value

investor are concerned not with the short-term technical pattern of asset

prices, but with the long-term value of their investments, which as we shall

show, are best expressed by the rates of return of bonds and by the implicit

rate of return of large, but riskier, portfolios of stocks. This analysis

therefore ties the contingent cash flows of the S&P 500 stock market

directly to the contractual cash flows of the bond markets and then shows the

former ought to be regarded as a markup upon the latter.

Historical

Difference Between Stocks and Bonds

In

portfolio management, stocks and bonds have traditionally been regarded as

separate entities. Stocks were for capital appreciation and bonds were for

income. Stocks have therefore been endowed with a separate aura from the more

traditional and staid bond markets. During the market crash of the 1929, the

stock and bond markets exhibited the following behaviors:

Table I

Comparison of

the Stock and Bond Markets

S&P Stock Index * Earnings/Share Corporate AAA

Bond Rate **

Year

(1941-1943=10) (adj. to index) P/E (Annual Average Yield to Maturity)

1928 24.35 1.38 17.64 4.55

1929 21.45 1.61 13.32 4.73

1930 15.34 .97

4.55

1931 8.12 .61

4.58

1932 6.89 .41

5.01

* “Standard

& Poor’s Security Price Index Record”; 1992 ed.; p. 120.

**

U.S. Census Bureau; Statistical Abstract of the United States 2003; No. HS-39.

If

you were a bond investor you did well enough. If you were a stock investor…. It

is also useful to note that the stock market crash between 1929-1932 was not

caused by an egregiously high market valuation. It was caused by a failure of

the entire international economic system after W.W. I.

Current

Similarities Between Stocks and Bonds

The

actual return of bonds held to maturity can be obtained directly from daily

quotes in the bond market, since bond cash flows are fixed by contract. What

makes the S&P 500, with a risk premium, nearly equivalent to a bond is the fact that it is diversified;

and linked both to the Fed’s monetary policy and to models that trade between

stocks and bonds.

Stocks

consist of 50 % of the U.S. securities market; and the S&P 500 accounts for

79% of that. The index is diversified among eleven industry groups. The Fed’s

administrative control of liquidity affects both the levels of the bond and

stock markets – most timely at this 11/22 writing. Moreover, the commonly used

Modern Portfolio Theory (MPT) model assumes stable average returns of stocks

and bonds, in order to then reduce portfolio risk. Given the above, we can

generally say that stock and bond returns are related.

Why

do we choose the S&P 500? There is also a very practical reason. Provided

its entry price is well chosen, (we are value investors), it is one of the best

long-term investments around, partaking of long-term innovation in the economy.

The 12th edition of Professor Burton Malkiel’s

book, “A Random Walk Down Wall Street (2020),” contains the following table:

Table II

Percentage of

Actively Managed Funds

Outperformed by Benchmarks *

One

Year Five Years Fifteen Years

All

Large-Cap Funds vs S&P 500 63.08 84.23 92.33

Global

Funds vs. S&P Global 1200

50.21 77.71 82.47

* Malkiel (2020); p. 177.

The

above table strongly suggests that over the long-term, index funds outperform

managed funds. The above is particularly relevant if you are interested in

other things besides markets and stocks. (We are fascinated by these, but

that’s us.)

We

think the long-term superiority of the index is simply due to its

diversification among different industries, and thus tricky sector rotation is

not necessary. Professor Malkiel writes, “Every time

I do a revision of this book, the results are similar (to the above).…(but)

What (Efficient Market Hypothesis) implies is that no one knows for sure if stock

prices are too high or too low.” (p.p. 177,181) So what we have is a outperforming asset, whose realized returns and volatility

(risk) are known, but whose price for a prospective required return is not.

It

is possible to use the principles of corporate finance to derive this price for

a single stock. It is also possible to use the same principles to derive the

required price for the S&P 500, with just one minor change in assumption.

It is then possible to compare the long-term returns of the S&P 500 at a

current or required price with those of bonds, whose prices are always known,

and to judge whether this is adequate for the future.

The

Value of the Future

The

MPT model assumes the future will be like the past, some kind of natural law of

average asset returns and Gaussian volatility having been discovered.

The

financial present value model values the future, in real markets. Neither model

nor real market can be “right,” and it is up to the investor to decide whether

the pricing available from real markets is reasonably right for him. The

reason for this subjectivity is simple. Bond markets, and thus interest rates,

vary all over the place; depending upon circumstances. Markets are sort of like

the Grand Central Station, where all economic influences converge.

It is a great advantage for investors to be able to

directly compare the return of bonds in actual markets to the return of the

S&P 500, a portfolio of stocks. We suggest a simple assumption, applicable

to large companies, that converts reported operating earnings according to GAAP

into cash flow. The simple assumption is this: annual capital expenditures (a

cost) approximately equals annual depreciation (an

expense). This simple assumption converts earnings into cash flow, that can

then be used to value the S&P 500.

S&P 500 Operating

Earnings

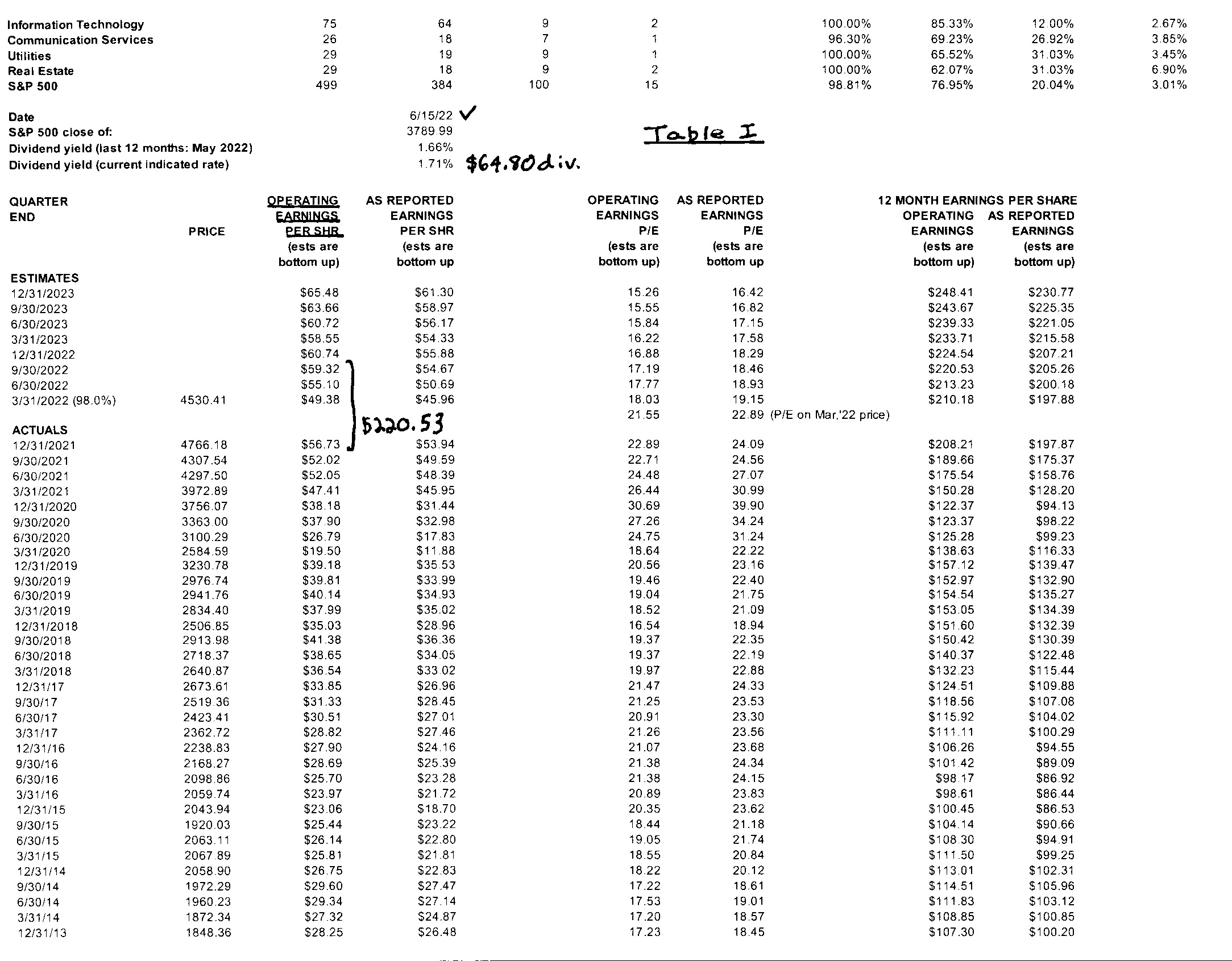

Standard & Poors

publishes detailed earnings estimates of the S&P 500, that is used in

finance as a diversified reference portfolio. Crucial to this, that we show per

S&P report, Table I,

is the distinction between “operating” and “as reported” earnings. One would

normally think of “operating earnings” as the direct costs on the factory floor

of producing goods, excluding corporate overheads such as interest paid on

debt, marketing costs, r&d and so on. However,

the intent of the S&P definition is to exclude only extraordinary items

such as fixed asset writedowns and gains or losses on

the sale of assets. This enables the summation of diverse company results into

a single figure, S&P 500 operating earnings that includes the cost of

leverage.

For large companies, yearly capital

expenditures approximately equals annual depreciation.

Therefore S&P 500 operating earnings approximately equals S&P 500 cash

flow available to shareholders. This emphasis on cash flow is crucial, because

it also enables the assumptions of company level corporate finance to be

applied to the valuation of the S&P 500. We can then simply capitalize

annual S&P 500 operating earnings.

The Operating Earnings

Yield Model

But how? Remember that the duration

(payback) period of a stock is approximately 36+ years. This implies that in a

fluctuating economy, one year earnings results, which

we will also discuss later, are less accurate than some form of long-term

average. In 1988, Yale economist Robert Shiller published “Stock Price, Earnings and Expected Dividends.”

Campbell and Shiller found, “Long historical averages of real earnings help

forecast present values of future real dividends (i.e. stock prices factoring out inflation).” This is the

famous CAPE (cyclically adjusted price-to-earnings ratio model). Those who are

further interested in how we derived the level of the S&P 500, or who would

like to do the calculation themselves, click here.

The 8/22/22 level of the S&P

500 is 4138.

The calculated level of the S&P 500

a/o 8/22/22 for a 7% annual return: P = (10

year average operating earnings/annual return) X 1.33

Ps&p

500 = (137.78/.07) X 1.33 = 2617

As we shall see, a 7% annual rate of

return is what is reasonably required to compensate investors for the long-term

risk of investing in equities.

The Gordon Model

It is a tenet of corporate finance that the total

value of the company to shareholders equals the present value of the stream of

dividends it produces, discounted at the rate of return required by investors

(a cost of equity capital to a company). For companies with a constant growth

in dividends, the Gordon model discounts those dividends back to the present.

Thus:

Ps&p 500 = __kE__ = .3573

X 220.53/(.07-.04) = 2626

( r – g)

P = price

k = the dividend payout

ratio=.3573 per NYU Stern School S&P statistics 2000-2020.

E = S&P operating

earnings=220.53 per S&P report, Table I. Calculated dividends

= $71.64. Actual dividends =

$64.80

r = the

rate of return of the investment=7%

g = the

rate of growth in dividends (earnings)=2% real + 2% inflation

We first encountered this model in a

stock market course; it struck us as very difficult to implement because what

do you assume for (r), what do you assume for (g), and where do you find (k)?

What this model requires is an interpretation in context, and that context is

the realities of real financial markets. As in the above, we assume for

economic growth 2% real and 2% inflation and that investment rates of return

should be a 1% markup over the 10 year bond rate of

return.

At a 7% rate of return, the two models

are within 0.34% of each other. We prefer the first model because it is

not dependent upon current dividend statistics. The dividend may be cut, as it was

in 2009, in the event of a severe recession. Both models show that

the current 8/22/22 level of the S&P 500 = 4138 is very unrealistic.

The Context of Markets

Both present value models need to

operate within the context of the economy and markets. On 8/22/22 here is how

equity looks according to the first model:

Table III

Logical

Expectation 8/22/22 Actual

Market 8/22/22

2% Policy Rate

2.33%

2% 10 year treasury premium

.70%

2% BAA

corporate bond premium

2.24%

1%* Equity risk premium (S&P

500=4138) ( .85%)

7% 4.42%

In response to Fed policy rate increases, the 10 year treasury is beginning to invert; and market traders

(and computers) are buying the dips. Markets are apparently assuming a return

of the low interest rate, low inflation, low growth environment of the past.

The Fed policy rate is currently way below the current 5.90% rate of inflation

in the core CPI, that excludes food and energy.

The Effect of Inflation

Another

advantage of a quantitative method to evaluate the S&P 500 is to analyze

the effect of unanticipated inflation. If the central banks were to tolerate a

4% inflation, rather than a 2% inflation, the further effect of this upon the

equilibrium value of the S&P 500 would, for most people, negate a

substantial lifetime of work.

8/22/22

current level of the S&P 500 = 4138

Predicted

level with a 2% inflation = 2617, 7% return.

Predicted

level with a 4% inflation = 2036, 9% return.

A

9% return sounds great, if you neglect inflation, but the predicted level of

the S&P must drop by another 22%; the factors ROC/R and LTG/R remain close

to their former values.

Portfolio

Spending

From

Keynes onward, it has been noted although stocks are clearly very long-term

assets, with a payback duration of over 36 years, their pricing in markets is

very short-term. If portfolios are structured

for the long-term, then a longer-term view is necessary. That longer-term

portfolio view, particularly for those interested in other things, is inflation

protected income – stocks for long run inflation protection.

The

bond markets, but not yet the stock market, are beginning to make it possible

for a 50/50 portfolio to reach a cash return of around 4%, which can be either

spent or saved. We are therefore now concerned with bond interest rather than

stock market dividends, which presently refer to a different world. The 4% rule

generally applies to portfolios managed in the U.S. or the U.K. which have

similar economic systems. This article

from the 5/8/15 NYT indicates that Bill Bengen, a

former financial planner and M.I.T. aerospace graduate, has worked out the

implications of this rule, with the provision that the future will be like the

past. In dealing with the present, this 4/19/22 WSJ article

writes that he is now mainly in cash. The rule-of-thumb is exactly equal to our

assumption for long-term economic growth – 2% inflation and 2% real. Stated in

terms of our model, the remaining balance of the portfolio (2% inflation and 2%

real) should last a long time, provided the U.S. economic system does not fall

apart due to great changes. Our 50/50 portfolio should eventually look like

this:

Table

IV

Asset Cash Return Weight Portfolio Cash Return

Bond 5.5% 50%

2.75%

Stock 2.5% * 50% 1.25%

4.00%

* S&P at 2617 a/o 8/22/22.

In real markets, we may be a few

10ths of a percent off; and the

S&P dividend level of $64.80

may be temporarily cut.

When

to Buy and Hold

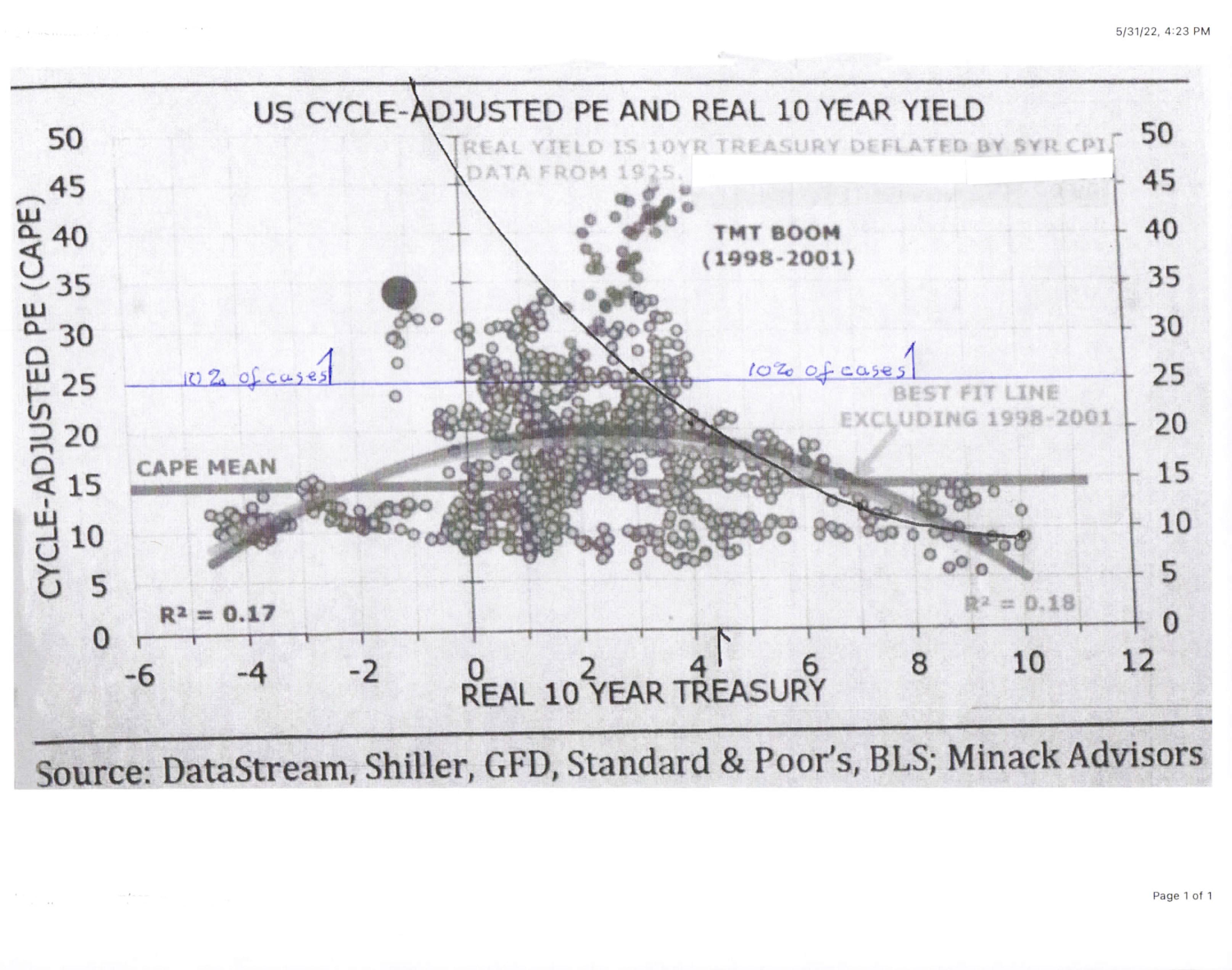

The

following graph from Minack Advisors is really useful, for it charts the entire

S&P 500 in terms of Professor Shiller’s cyclically adjusted earnings model. It shows that most of

the time, say 90%, the conventional mantra of staying invested and adding to

one’s stock investments is correct – when the cyclically adjusted P/E is less

than 24. But when the CAPE P/E is greater than 24 (10% of the time, and

provided the economy does not change drastically from the past) we would not

add to our stock holdings and would think of trimming back; even though the

market might be soaring. With inflation now out of control, we are now in the

throes of a large market correction.

Conclusion

This study places the S&P

500 in the context of the bond markets, and thus its prospective rate of return

to investors. We hope that this has been helpful to you.

We encourage you to speak

with a qualified financial advisor about your specific situation.

{kind=link}

{kind=link}

{kind=link}