1/1/19 –

On

12/31/18 the S&P 500 closed at 2507, resulting in a total return of -4.38%

for the year. According to the November, 2018 Fed Open Market Committee, “…the labor

market has continued to strengthen and that economic activity has been rising

at a strong rate.” This observation correlates with the fact that, while bank

lending was stagnating

prior to the Great Recession of 2008, lending is now growing strongly.

But

in the month of December, the S&P 500 declined by 9.1%, a worse December

performance than the 6.0% December drop in 2002, giving investors a lump of

coal in their stocking. The 12/24/18 NYT notes, “…the biggest worry for 2019 is

not so much that…disruptions (are) so large to cause a recession. The real fear

is that shaky policy allows small shocks to create a broader crisis of

confidence.” For both the real and financial economies, confidence matters.

In

The General Theory (1954) Keynes

wrote, “The state of confidence…is a

matter to which practical men always pay the closest and most anxious

attention. But economists have not analyzed it carefully and have been content,

as a rule, to discuss it in general terms….There is,

however, not much to be said about the state of confidence a priori. Our conclusions must be mainly depend

upon the actual observation of markets and business psychology. This is the

reason why the ensuing digression is on a different level of abstraction from

most of this book.”

The

practical reasons for having confidence are surely the elements of intention,

competence and reliability. What does it mean to have confidence in government,

particularly the competence and reliability of Fed policy? In a 12/21/18 CNBC

interview, John Williams, president of the New York Fed, crucially remarked:

1) The Fed seeks the best policy, to achieve

its dual mandate of high employment and low inflation.

2) In developing this policy, it looks at the

incoming data and, most crucially, talks to many others.

3) As a result, the Fed “judges” rather than

“expects.”

The

underlined words are the crucial elements of rationality under the condition of

uncertainty. (Hopefully) with our readers, we now discuss what rationality is.

The

most general definition of rationality is to do things for reasons, to obtain a

given result. A more specific definition of rationality depends upon the

conditions under which it occurs. Ref. (Russell and Norvig, 2010). For

instance, when driving to a destination, a fog might roll in. Depending upon

the degree of fog, one can look at different things to reach one’s goal.

1) On a clear day, there are no other vehicles, the

environment’s landmarks are clearly visible; and one can drive along the best

route with almost no other feedback. This is navigating under certainty.

2) The fog begins to roll in, there are no other

vehicles, the environment’s landmarks are visible only in blurry outline; the

prudent thing to do is to slow down and to verify that the landmarks are the

actual ones. This is navigating under risk, when the alternatives are known but

the probabilities of their realizations can be identified estimated * by

numbers ranging from 0 to 1. The action to take is to proceed along the best expected

route.

3) The fog becomes pea-soup thick, there are no

other vehicles, the landmarks appear sporadically, the smart thing to do is to

slow down more and to ask the expert passengers to help identify the landmarks.

This is navigating under uncertainty, where the alternatives must be identified

anew in a complex world. Under these conditions, taking the best route requires

good judgment, consultation with other experts and continued

communication in a “multi-agent environment.”

This

discussion shows that Reason can be a very powerful tool – when reasonably used

after considering conditions.

*

This is a very crucial distinction. In the practical world, good judgment is

really important. Russell and Norvig (2010) write, “The connection between

toothaches and cavities is just not a logical consequence in either direction.

This is typical of the medical domain as well as most other judgmental domains:

law, business, design, automobile repair, gardening…” The title of their

definitive book is, “Artificial Intelligence.” It discusses A.I. algorithms and

design considerations, also philosophy from Aristotle to Gödel, in 1132 quite

difficult pages.

What

is useful to us is that computer programming forces clarity upon some questions

that originate in the humanities; A.I. is likely to have a very large impact on

society. However, this is not at all to reduce one field to another.

__

At

the 1/4/19 annual American Economic Association meeting in Atlanta, Fed Chair

Powell and former Fed Chairs Yellen and Bernanke placed the implementation of

Fed policy in the perspectives of the U.S. and world economies.

1.

Powell:

The Fed will be patient and flexible in its implementation of monetary policy.

The U.S. economy is growing moderately and well. In December jobs increased by

312,000 (our note: about 170,000 is normal), unemployment has been less than 4%

for four months, wages are moving up along with labor participation.

The financial markets, however, foresee

the opposite. With China pulling back, copper down. The financial markets are

pricing in downside risk to global growth. We don’t have a fixed monetary

policy. In the 2016 (international) taper tantrum, Chair Yellen nimbly adjusted

rates and normalization resumed. We will be prepared to adjust policy quickly

and flexibly.

We need the concept of the natural

rate of unemployment, to give us an idea of whether interest rates are too

high, too low or just right. The exact level of the natural rate is uncertain,

but it is possible to go too fast in relation to resource constraints.

Future research ought to integrate

macroeconomics (our note: assumes equilibrium) and markets (our note: assumes

disequilibrium on the path to equilibrium ).

2.

Yellen:

We have a strong economy with consumer spending comprising 2/3 of it. The

Philips curve (linking unemployment and inflation) is relatively flat, giving

the Fed the opportunity to move carefully in a data dependent manner, managing

risk. The growth rate of the economy is consistent with potential and may

warrant some tightening.

When giving rate guidance, it will be

important for the Fed to co-ordinate across asset classes.

3.

Bernanke:

It was very important for the Fed to anchor inflation expectations at 2%. As a result the Philips curve is flat, allowing the Fed to

experiment with policy. Unanchored inflationary expectations mean that it is

more difficult to stabilize the economy.

(This is really important because it

provides an order that enables a rational and more deliberate management of the

economy.)

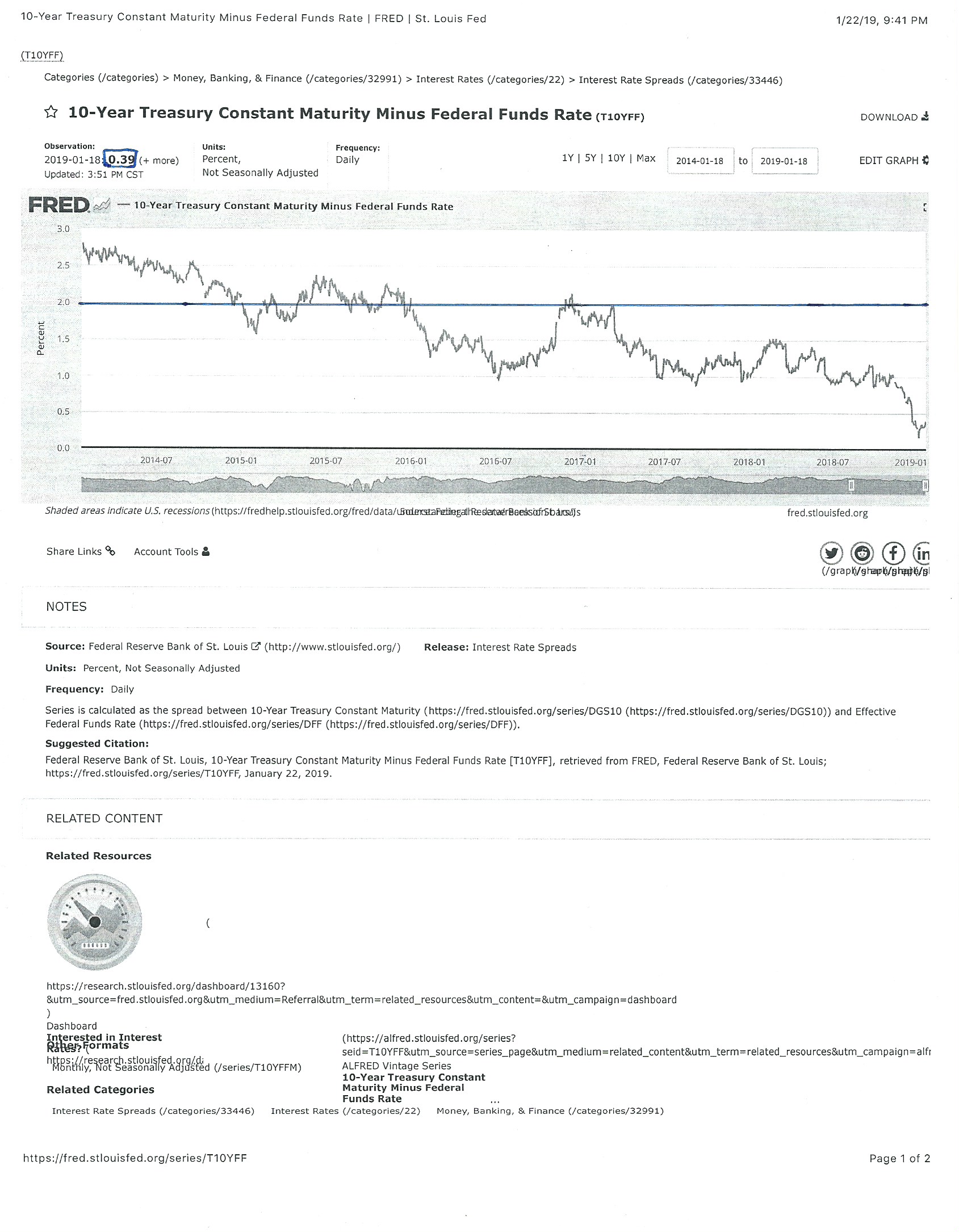

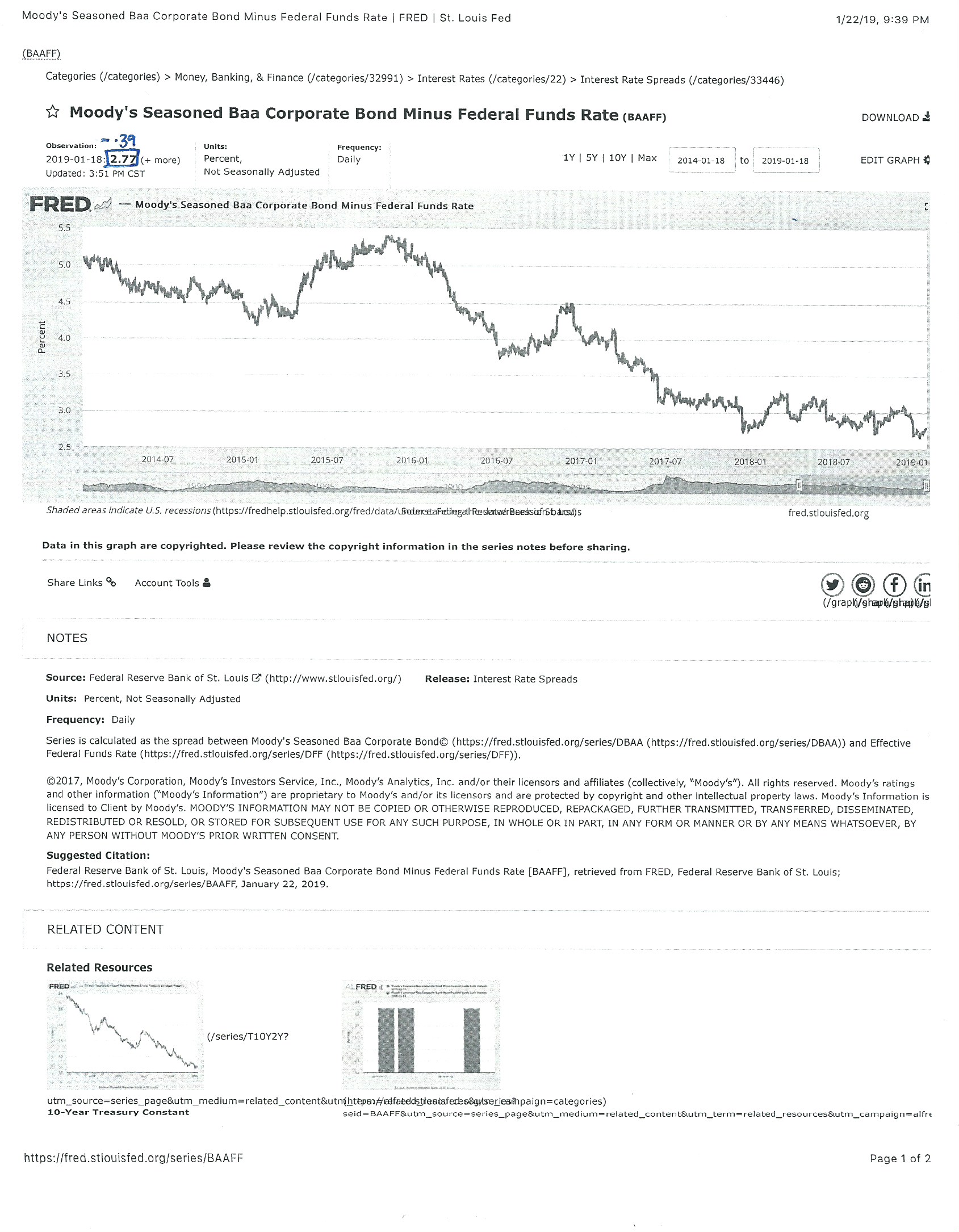

2/1/19 –

On

1/18/19, the S&P 500 closed at 2671, providing a long-term investment

return of only 5.3%.

The

pricing of assets in the financial markets is based upon a risk markup from the

short-term Fed policy rate, currently at 2.5%. Under normal spread conditions,

the rates of return available from major financial investments are as follows:

Normal Conditions

Current Conditions

2.5%

Policy rate

2.5% Policy

rate

2.0% 10 year treasury premium

.4% 10 year treasury premium

{kind=link}

2.0% Corporate

bond premium 2.4% BAA corporate bond

premium

{kind=link}

2.0% Equity risk premium 0% Equity risk premium

8.5% Normal equity

return * 5.3% Equity return 1/18/19**

* With the exception

of the policy rate, these are returns available under normal conditions. For

the ten year bond, a rule of thumb is 2% above the

policy rate.

**

The present ten year treasury premium of only .4%

signals a flat yield curve and a low demand for capital either due to low

growth (and the increased digitization of the economy) and/or an impending

recession. The high BAA minimum investment quality bond spread signals a

recession. The equity return of 5.3% assumes a

cyclically adjusted 10 year S&P 500 operating earnings average. Growing

this year’s earnings estimates in perpetuity would result in a much higher

equity return.

But

why is the equity risk premium zero (which is another way of saying the

stock market is overvalued)? *** In theory, equities are supposed to be more

risky than corporate bonds; but financial history is what actually happens.

During the last ten years, the economy has been slowly recovering from the

Great Recession, when rates were at the zero bound, overvaluing equities, which

do not default the way bonds do. At a zero required rate of investment return,

the price of an infinite stream of $1 payments is infinity. With rates low

since the Great Recession of 2008, and just beginning to normalize, equities

have been overvalued.

If

this economic recovery continues, the Fed will very likely raise interest rates

slowly, in a conditions dependent manner, to stabilize inflationary

expectations and keep the real economy’s expansion going. If the economy slips

into a recession due to a combination of factors affecting business confidence

such as the shutdown of the Federal government and/or financial crises abroad,

with a trillion dollar government deficit right now,

future monetary policy is less likely to be effective. There will also be

balance sheet (stock) problems that go beyond the decreased (flow) of exports.

Equities will unlikely remain at a “permanently high plateau.”

***

Jagannathan, McGrattan and Scherbina (2000) from the

Kellogg School and the Minneapolis Fed found that the equity premium relative

to 20 year U.S. long-term government bonds in 1999 was

-0.27%. Our calculation yields a present equity premium of 2.4% against 10 year government bonds.

The

spreads above obviously vary according to financial conditions. It is possible

to read the story of the markets from these spreads, and to ask whether the

spreads justify the individual asset risks.

__

With U.S. economic growth still continuing, this is the

time to seek reforms, to begin to solve many problems that only government can

remedy. In his epic chronicle of the French Revolution of 1789, Citizens, Simon Schama writes that the ancien regime, distracted by modernization

and unable to effect financial reform, frittered away its social order in

discord – often incited by members of the aristocracy. The result was prolonged

chaos. Writing On The Origins of War,

the classicist Donald Kagan noted that the next generation of European

statesmen then constructed an international treaty system that resulted in

decades of peace and stability, a stability that vaunting national ambitions

increasingly undermined prior to W.W. I.

The

rest, as they say, is history. The 1/22/19 NYT

reports that a major investor now warns against, “global social tension, rising

debt levels and receding American leadership.” Social stability should not be

taken for granted. U.S. social cohesion is quite challenged by a “whatever it

takes” culture in business and politics.

3/1/19 –

On

2/25/19 the S&P 500 closed at 2797, providing a long-term investment return

of only 5.10%. Asking for a 8% investment return in a

5.10% world might seem unrealistic. But the market is presently assuming business

as usual: Agreement on all substantive trade issues with China; Britain

negotiating an acceptable Brexit deal; interest rates remaining low for the

duration (payback period) of the S&P 500, around 36+ years.

Two

protections we have against the above uncertainties are:

1)

Requiring

a higher rate of return on the S&P 500 to compensate for the above risks

and those developing.

2)

Considering

the future, with its risks - although interest rates in Europe remain very low,

the bias in the United States is likely towards slightly higher interest rates

to keep control of inflation in a growing U.S. economy. At some time, we will

probably begin to lock in bond returns before stock returns; bonds are

shorter-term assets than stocks.

The

present overpricing of equities is due less to “irrational exuberance,” but the

result of generally low interest rates (if you consider a low discount rate

capitalizing a perpetual stream of S&P 500 operating earnings). In “The General Theory (1954),” Keynes

wrote, “In practice we have tacitly agree, as a rule, to fall back on what is,

in truth, a convention. The essence

of this convention – although it does not, of course, work out quite so simply

– lies in assuming that the existing state of affairs will continue

indefinitely, except in so far as we have specific reasons to expect a

change.”

_

Portfolio

Notes

(1) Unlike the

analysis of individual financial markets, the goal of quantitative portfolio

management is to evaluate the risks and returns of individual financial assets

(so calculated) to match the risk and return of an entire portfolio (so

calculated) to the requirements of the owner.

The

following is what we intend to do at this time. We definitely encourage our

readers to consult with their qualified investment advisors to discuss how

their unique financial situations should determine an appropriate portfolio

structure.

A

major input into a quantitative analysis of portfolio management is the concept

of average portfolio returns. But:

1)

In

volatile markets, cumulative portfolio returns will be lower than average

returns. The value of a portfolio that increases for two years at a steady

state of 6% per year will be $112.36. In a very volatile market, the value of a

portfolio that increases by 50% in the first year and then decreases by 38% in

the second year will be only $93.00. In both cases, the portfolios will have an

average return of 6% per year.

2)

A

prolonged period of very low or negative portfolio returns can cause a

portfolio to run out of money, even though the returns of subsequent years are

very high.

Considering only average

portfolio returns is very misleading. There are two fundamental principles of

traditional portfolio management that investors should bear in mind:

1)

In

normal (we’ll get to this later in the case of stocks) markets, portfolios

should be structured with high-quality asset classes bearing a lower degree of

risk.

2)

Draw

down the portfolio only to the extent of income, not drawing upon “principal,”

to which the present value formula is agnostic.

As an example, we consider the income

implications of a conservative 50/50 S&P 500 stock portfolio and two

intermediate maturity mutual fund bond portfolios. In practice, we will phase

in our investments in these assets, and realized income yields will differ somewhat

(investors propose and the markets dispose) from the below:

Asset Weight Income Yield Weighted Income Duration (years)

S&P 500* 50% 3.0% 1.50% 36 +

Bonds ** 50% 3.5% 1.75% 6.1 -

3.25%

* Return of 8%

rather than current return of 5.1%

**Return of 3.5% rather than a

current return of 3.1%

We think a global add: In the short-term, a U.S. low interest rate environment, with

possible excursions to the zero bound, is much more likely than a high

interest rate one - due to globalization and digitization where many services

have become virtual. This is our take. During 1970s, inflation and thus very

high interest rates were caused by much more localized economies enabling, we

think, a few producers (including of course OPEC) to cause high inflation by

their price hikes. Markets now, particularly the labor markets, are much

broader.

The

major risk to portfolios is therefore prolonged recession, causing interest

rates to again reach the zero bound. We will therefore lock in bond yields

before stock yields. Conversely, if interest rates increase drastically, a 6.1 year duration bond portfolio is much less risky than a

36 year duration stock portfolio.

(2) This figure graphs * long-term government

bond yields in five developed economies. It illustrates that since 1990 there

has been a precipitous decline (but a present slight rebound) of interest rates

and thus financial asset returns due to structural and technological changes in

the world economy. As a result, investors in search of high returns, have been

taking increasing risks – 2008 was a frenzied peak of this. We will be taking some

credit risk (but the mutual fund bond portfolios we are considering each

contain more than 1500 – hopefully not highly correlated – bonds). These two

portfolios will also average out to around 25% U.S. governments. If we can get

a 3.5% income yield with a single bond portfolio containing 50% governments,

all the better. We think that would be a bargain in the risk space.

We carefully chose ten highly rated

corporate bond issues in our own portfolio (there is an advantage to holding

individual issues because the duration and therefore interest rate risk of the

bond portfolio will decrease over time). But several years later, the ratings

agencies drastically downgraded a bond we had already sold. The company had

made bad acquisitions that drastically reduced its margin of safety. Like stock

portfolios, bond portfolios also need to be diversified and monitored.

*

This graph is in .pdf file form. If you don’t have Adobe Acrobat: In the 1990s

government bond yields ranged (12%-6%), in 2019 they are now (3%-0%).

On

3/22/19 the S&P 500 closed at 2801.

The

economic slowdown in Europe and the rest of the world is beginning to affect

the U.S. markets. The European governments did not quickly deal with their

problem bank loans the way the U.S. government dealt with its problem bank

loans (with the Tarp programs that ended in 2014, netting a $15.3 billion profit).The

3/22/19

WSJ quotes, “(The banks) have been slow to clear their balance sheets of

problem loans and so are unable to help the economy grow…In Europe, you end up

still with hundreds of billions of bad loans on bank balance sheets more than

10 years (sic) after the crisis and that restricts growth.” As a result, German

bund yields are again negative and that drags down U.S. treasury rates, causing

low returns in all U.S. asset classes and…(we noted

above) affecting the feasibilities of structuring portfolios that will provide

decent returns for the future.

The

WSJ article further notes, “The fall in European yields has put pressure on

U.S. yields as investors starved of returns in Europe are moving into Treasurys. Investors’ other option is to take more credit

risk (finance calls this ‘a reach’) by buying lower-quality debt or longer-term

bonds. Investors are left confronted with a conundrum…either accept a definite

small loss from a negative yield, or take risks that could lead to bigger

losses.”

This

is essentially the dilemma that all investors face; because the productive use

of their savings to generate income depends upon the health of the future

economy. This, as the following also suggests, can occur only in a

well-regulated system - not in someone’s vision of a totally unregulated and

therefore uncorrected markets. In the present financial environment, we aren’t

taking large risks until the market pays us to.

_

The

climate, like markets, is a natural phenomenon. Like gusts of wind before a

hurricane, the effects of global warming are beginning to be manifest; Cyclone Idai displacing hundreds of thousands of people in

Mozambique, Zimbabwe and Malawi; as floodwaters recede in the Midwest, NOAA

expects that nearly two-thirds of the lower 48 states face an elevated risk of

flooding through May; the 2018 wildfire season in California resulted in a

record total of 8,527 fires burning an area of 1,893,913 acres.

Our

next essay, “Climate Change and the Economy” will discuss the scientific

evidence for taking action to control global warming, if we are to have a livable

future. The larger effects of global warming will take effect in at least ten

years, well within the 36+ year duration of the S&P 500.

Although our financial asset buy points remain the same, we do think it is appropriate to

be slightly more cautious in our planned asset allocation because effective

political responses to global warming have yet to occur.

5/1/19 –

During

a European financial crisis, we were analyzing a European bank credit. What

would happen, we asked, if the European banking system collapsed? The level-headed response was, “If that

happens, we’re all in trouble.”

In

the face of global warming, we think this is the appropriate attitude for a

long-term investor in a climate challenged world. Our strategy will be to hold

a steady course, paying special attention to portfolio risk structure,

valuation, and to rely on the managers of partially U.S. government bond

portfolios (with an average maturity of around 8 years) and the turnover of the

S&P 500 (now forecast by Inc.to

decrease to 14 years by 2026) to make the appropriate adaptions. This

crucially assumes that governments will act to protect their peoples and their

investors from the worst effects of climate change. If governments do not

act to limit catastrophic levels of CO2 ,

investors need not consider whether their then abstract net worths

matter in relation to other more basic needs, like food and water. What follows

is a further discussion of the science of global warming and the likely

efficacies of its remedies.

In

the history of life on earth, there have been five large life extinctions, all

caused by excess atmospheric carbon, resulting in global warming. Of the five,

one was greatly exacerbated by a large meteor that eliminated the dinosaurs at

the end of the Cretaceous period 66 million years ago. The other four were

likely caused by the carbon dioxide belching from large fissures (most notably

during the Permian period that formed the current Permian basin in Texas) or

triggered by the release of methane, also a greenhouse gas, from the sea floor.

Of special interest to climate scientists is the Paleocene Thermal Extinction

which occurred 56 million years ago, when the dominant animals were large

carnivorous birds (descended from their dinosaur ancestors) and animals such as

smaller birds, mammals, amphibians and insects.

56

million years ago, the concentration of atmospheric carbon dioxide was around 1,000

parts per million; the current concentration is around 406 ppm and rapidly increasing. According to the 3/27/18

Washington Post, “To many scientists

today, many of the phenomena observed during (that period) will feel familiar –

so familiar ‘it’s almost eerie,’…Humans burning fossil fuels have produced the

same kind of carbon isotope spike researchers find in 55-million-year-old

rocks. The ocean has become about 30 percent more acidic and it’s losing oxygen

– changes that are already triggering die-offs. The world has witnessed

dramatic weather extremes – deadly heat waves, severe storms, devastating

droughts.” At that time, the Antarctic ocean was about 68 degrees Fahrenheit.

The tropical temperature off the coast of West Africa (the changing continents

were in slightly different positions) was 97 degrees. Needless to say, these

torrid conditions caused extinctions. It should also be noted that there was no

ice on earth at that time, to become unfrozen. “In all major ways it’s more

perilous now then it would have been then…”

{kind=link}

As

with A.I., the key factor determining the future is human agency. Whether we

will survive the effects of global warming depends on what people collectively

do, acting through the agency of government. Substantial global warming will be

a fact, but there are two major carbon pathways of handling global warming;

both require the actions of governments.

The

first pathway is might be called the “consensus” pathway. As described

by Vox and advocated by Shell Oil and

some other unaffiliated researchers, it sets forth a pathway to 2° warming and zero emission growth by 2070 assuming a

continued high growth in energy consumption, up 237% by this date, and also

assuming in main:

· Carbon pricing

mechanisms adopted by governments in the 2020s, leading to a meaningful cost of

CO2 embedded within consumer goods and services.

· A rate of global

electrification reaching a level nearly five times today’s level.

· New energy sources

grow up to fifty-fold with primary energy from renewals.

· A change in the

efficiency of energy use leading to gains above historical trends.

· And most

heroically, some 10,000 large carbon capture and storage facilities, compared

with fewer than 50 in 2020.

The

report however then says, “…achieving net-zero emissions in just 50 years

leaves no margin for interruption, stalled technologies, delayed deployment,

policy indecision, or natural back-tracking.” In other words, everything has to

go just right. The deus ex machina in all this is, writes Vox, “…we can exceed 2° C some time

mid-century (known as “overshoot”), but then pull enough carbon out of the

atmosphere in the latter half of the century to restore balance and pull the

temperature beneath 2°.” The problem is that that carbon sequestration

technology is presently unproven at scale; it would be a rash to gamble the

fate of your families on this unproven technology. Worse, considering climate

complexity, the non-linear effects of global warming are likely to be much more

manifest by then.

The

second pathway is the practical one. In 2015, 195 nations signed the Paris

Agreement, with the goal of holding global warming below 2° compared to

pre-industrial levels. In 2017, President Trump announced the US withdrawal

from that Agreement in 2020. The 2017 UN Environment Program Emissions Gap

Report writes, “The overarching conclusions of the report are that there is an

urgent need for accelerated short-term action (starting right now)…if the goal of the Paris Agreement is to remain

achievable – and that practical and cost-effective options are available to

make this possible.” We think that these options are the best alternatives

because, “…(they) can be implemented at relatively low cost and based on significant

existing experience. Together they represent more than half of the

(reduction) potential identified.” The message is that there is still time; but

there is no longer a free lunch in environmental matters because Mother Nature

is starting to react badly.

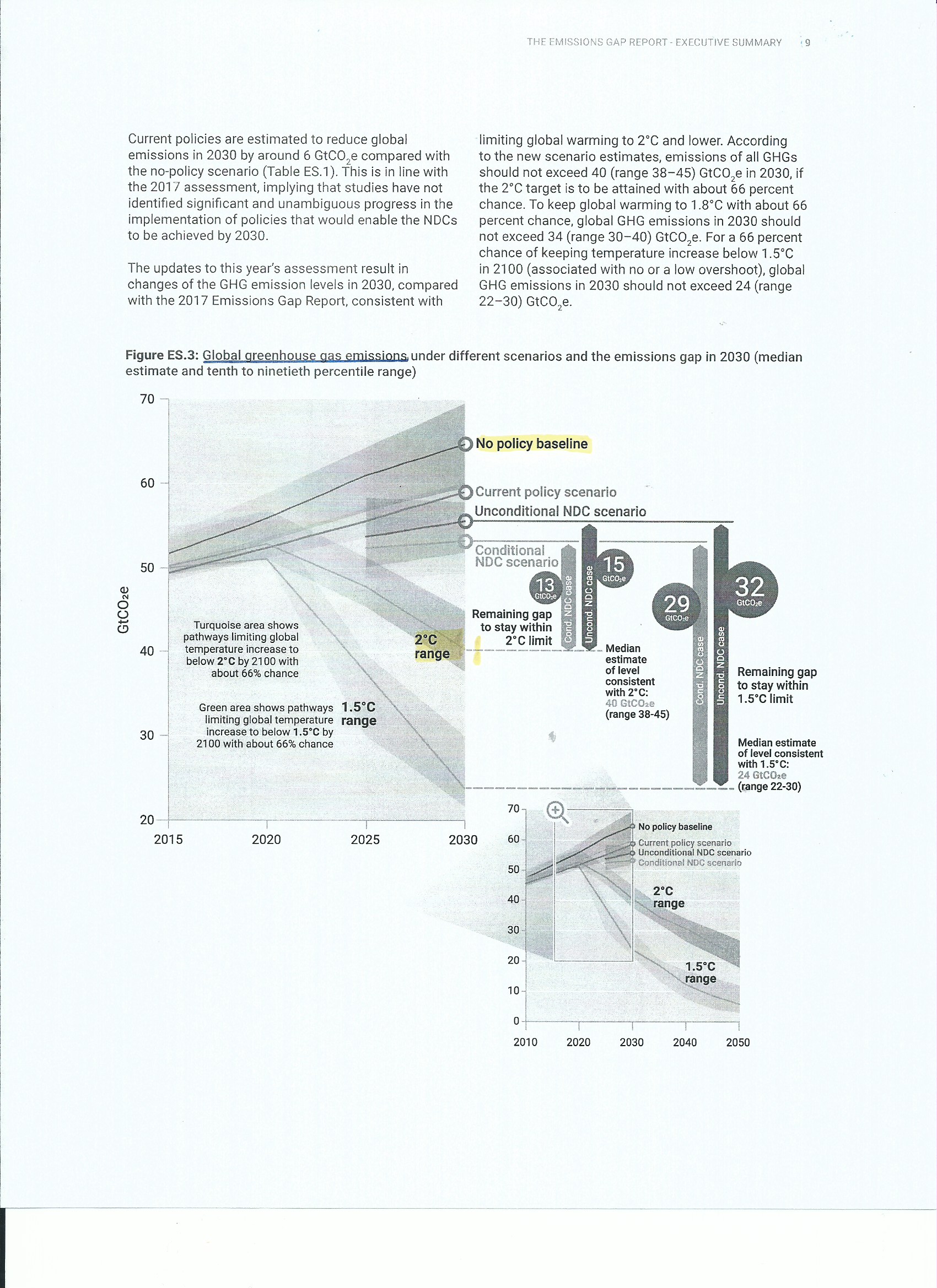

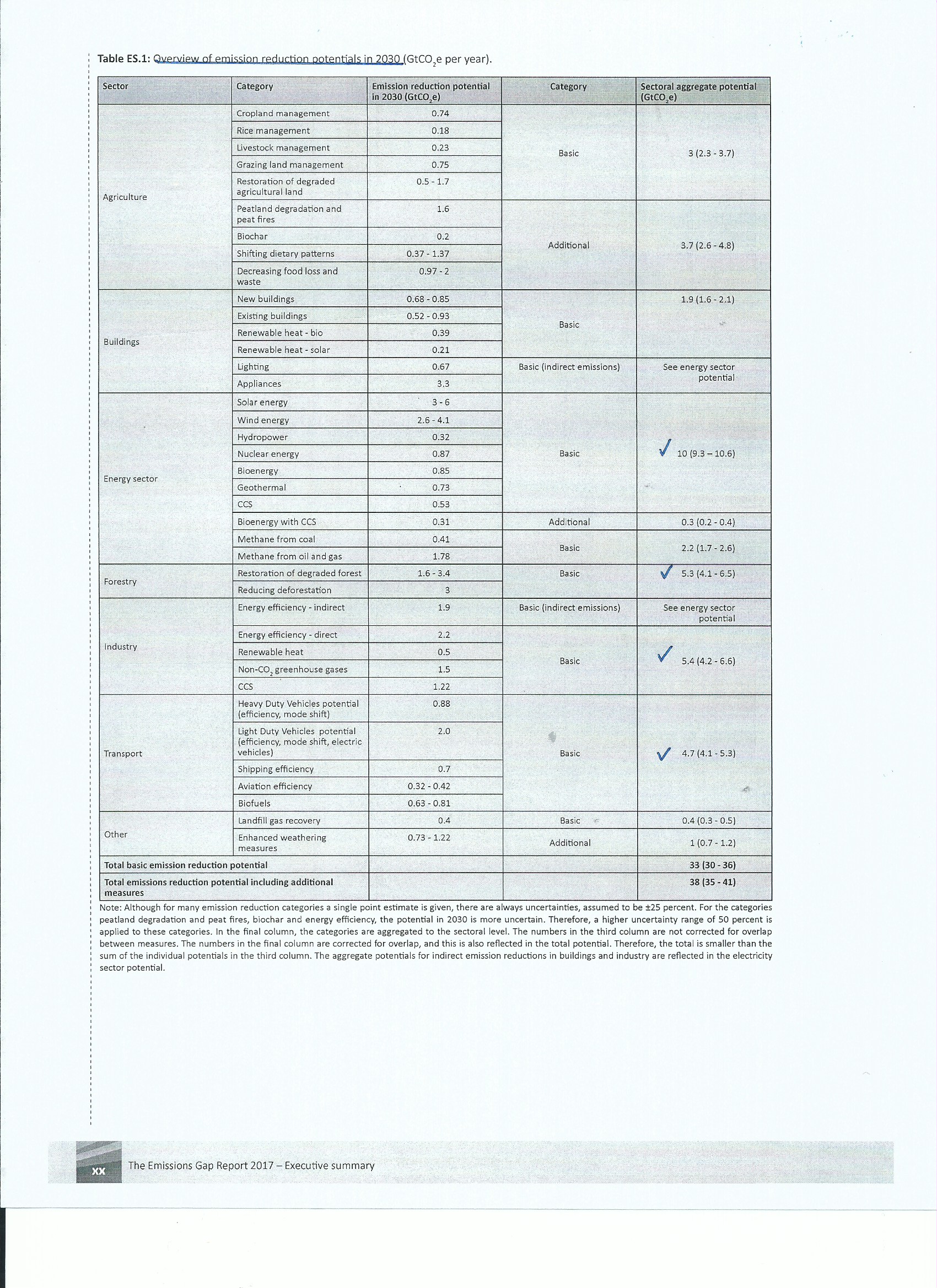

The

2018 UN report graphs the

world’s greenhouse gas emissions in units of billions of tons of C02.

* This graph shows to achieve at least a 66% chance that global warming will be

2° C or below by 2100, CO2 emissions will have to drop from around

52 billion tons at present to 40 billion tons by 2030, a decrease starting

right now of around 12 billion tons or 23%. (Note that Shell, of course,

projects a large increase in energy use.) This table shows that the major

world-wide potentials for cost-effective emissions reduction are in the energy

sector (10 billion tons), industry (5.4 btons),

forestry (5.3 btons), and transport (4.7 btons). The total emissions reduction potential of these

and other measures is 33 btons of CO2.

Since these figures are from a large number of sources and utilize existing

technology, the worst of global warming can be avoided. But it is necessary

to act now.

{kind=link}

{kind=link}

How

to make greenhouse gas reductions happen?

·

Reaffirm

the Paris Climate Agreement, and then work with other countries to improve it.

·

The

media can play a very large role in publicizing the increasing effects of

global warming and increasing the public's undersanding

of this issue, informing how it will affect them. A detailed 3/21/17 NYT article

notes a Yale survey; 75% of the U.S. public support CO2 reduction.

·

Organize

broadly to affect the political process. There are committed climate change

deniers on the other side, like the Tea Party and some business interests, that

can take candidates out in the Republican primary.

On

4/18/19 the Justice Department issued a redacted Mueller Report,

chronicling the President’s attempts to end Robert Mueller’s investigation and staff

resistance to these. But when the histories of this time are written, they

will likely record that the worst mistake of the Trump administration and the

Republican party was to deny global warming. The election of 2020 will really

matter, for the future of your family and your investments. Elections have

consequences.

↓ We

Also Suggest ↓

6/1/19

-

On 5/23/19 the

S&P 500 closed at 2822, yielding an annual 5.26% return to long-term

investors. In order of increasing risks, the following returns are available in

the financial market on 5/23/19.

Market Premiums on

Offer

2.50% Policy rate

-.07% 10 year treasury premium

2.28% BAA

corporate bond premium

.55%

Equity risk premium

5.26% Equity

return

What’s wrong with

this picture?

What’s wrong with

this picture is that after ten years of slow economic recovery, the market

assumes that the future will be just like the past. The market assumes that

there is no duration risk in the 10 year bond market

and that there is no risk in equities, with a 36+ year duration (payback

period), over BAA corporates. In the words of a treasury bond columnist,

treasury bonds currently offer “return-free risk.”

Portfolio

Structure

If the purpose of

the analysis is to structure a portfolio whose income drawdown will enable it

to last for decades, the conclusion is similar to the above. In specific, if an

investor’s portfolio is conservatively structured 50% 10 year

treasuries and 50% with a S&P 500 index fund, the income yield of the

entire portfolio will be only 2.185%. Put another way, the portfolio must have

a principle balance 45.8 x the annual income drawdown –which is unrealistic for

all except a very few.

On the other hand,

if better terms are available in the financial markets to investors, say a 3.5%

yield on ten year treasuries and a 3% dividend yield on the S&P 500

(corresponding to a 8% return on the S&P 500), a blended 50/50 portfolio

will have an income yield of 3.25%, and

require a principle balance 30.8 x the annual income drawdown – which is still

above the 25 x (4% income yield portfolio rule-of-thumb) but a lot more

feasible than the above.

Investment Risk

and Return

If the purpose of

the analysis is simply to ask whether the 5.25% long-term return of the S&P

500 rewards investors for the risks we shall discuss, the answer is definitely

negative, unless you are a trading computer.

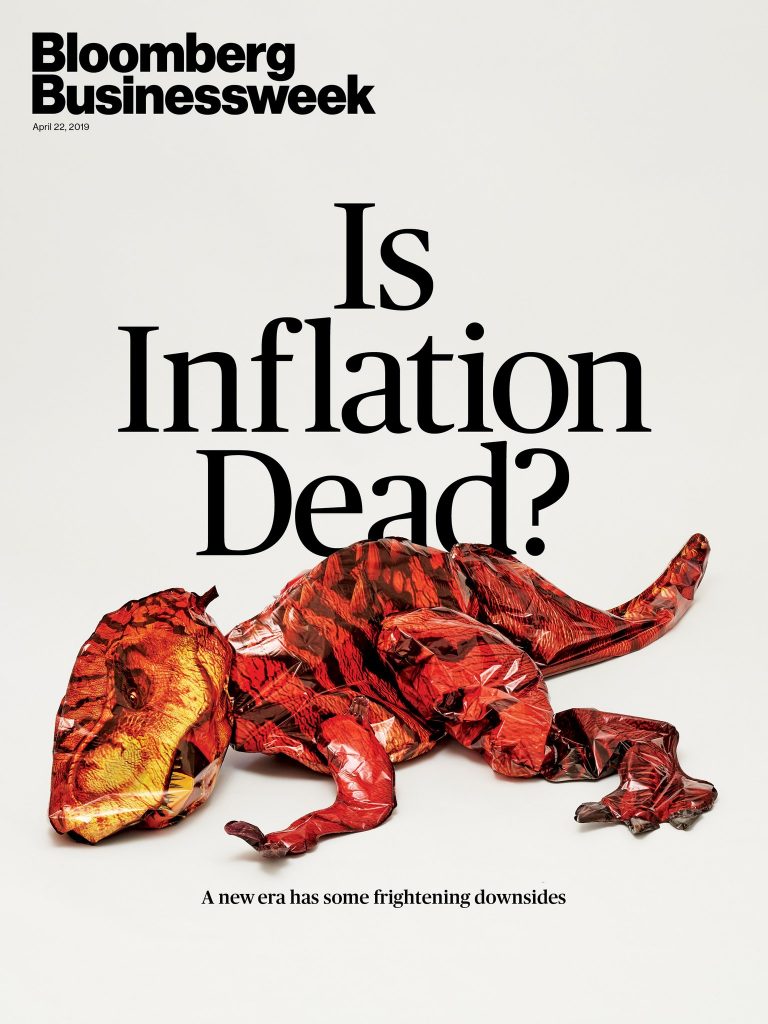

Risks

Investors face

three major risks that interest rates will increase over the short, medium and

long-terms. The April 22, 2019 issue cover of Bloomberg Businessweek shows a deceased T. Rex under the

caption, “Is Inflation Dead?” The article assumes the continuation of low

inflation, “…in large part (due to)…globalization or automation or deunionization-or a combination of all three-which undermine

workers’ power to bargain for higher wages…the major industrial economies will

be stuck with low inflation and low interest rates ‘for another 10 to 15 years,

at least.’” This is the “secular stagnation” hypothesis.

{kind=link}

But consider a

5/3/19 quote from Warren Buffet. “I can’t reconcile a five percent budget

deficit in a world of low unemployment, low interest rates, negative interest

rates in many countries. No economic textbook I know that was written (in) the

first couple thousand years discussed even the possibility that you have this

sort of a situation continue and have all the variables stay more or less the

same. So, I think of change. I don’t know when. I don’t know to what degree. I

don’t know what part of it’ll change. But I don’t think this can be done

without leading to other things….And we will look back

at this period and be surprised that we didn’t see what was coming next.”

Over the short

term, consider Trump’s trade war. It will be equivalent to a partial

depreciation of the dollar, adding to the cost of consumer goods in the U.S,

thus increasing inflation in an economy already operating close to capacity. At

the same time, this could also lead to a decrease in economic growth – a

difficult combination of events, last experienced in a much more severe form

during the OPEC era of the 1970s.

Over the medium

term, consider the need of the U.S. to reinvest in its own society. The capital

markets currently do not appreciate investor capital,

thus rates are low. But the U.S. must increase its investment in infrastructure

(Rated D+) 1, Education (37 countries had higher 2015 PISA math

scores and 23 had higher language scores) 2 and improve both the

efficiency and coverage of the world's most costly healthcare system (16.9% of

GDP) 3. Investing again in our society will cost money, likely

leading to a higher demand for capital and higher interest rates.

Finally, over the

long-term (say beyond the next 7 years or so), consider global warming. Since

it is likely that the average global temperature will increase beyond the 1.5° C over the preindustrial level targeted by the Paris

Agreement, the result will be increased capital expenditures to remedy climate

damage. The global temperature increase is already more than 1° C and rapidly

rising due to positive feedbacks, for instance the differences between ice

cover reflectivity and bare rock heat absorption. Also, there will be a large

number of “stranded assets,” as global warming obsoletes a large amount of

capital equipment, which must be replaced. 4

Dealing with

change, social system problems and global warming will require much social

cooperation. There is still time, but the window is rapidly closing. Our next

essay will discuss, “What Must Be Done”.

1

Washington Post, “Trump falls short

on infrastructure after promising to build roads, bridges and consensus”,

5/26/19.

2 Pew Research

Center, “U.S. students’

academic achievement still lags that of their peers…”, 2/15/17.

3

Americashealthrankings.org, ”Comparison with

Other Nations”, 2016 Annual Report.

4 add:

The 6/4/19 NYT writes, “Many of the

world’s biggest companies, from Silicon Valley tech firms to large European

banks, are bracing for the prospect that climate change could substantially

affect their bottom lines within the next five years, according to a new

analysis of corporate disclosures. Under pressure from shareholders and regulators,

companies are increasingly disclosing the specific financial impacts they could

face as the planet warms, such as extreme weather that could disrupt their

supply chains or stricter climate regulations that could hurt the value of

coal, oil and gas investments. Early estimates suggest that trillions of

dollars may ultimately be at stake.”

add: Concerning the obsolescence of a

large amount of capital equipment, consider this 6/6/19 NYT article.

“The internal combustion is under attack from electric challengers. Car

ownership is becoming optional in the age of Uber. Regulators around the world

are fining companies that don’t do enough to cut CO2 emissions even as buyers

demand gas-guzzling S.U.V.s…New technology has unraveled industries like

entertainment, media, telecommunications and retailing, weakening the job

security of millions of workers and helping to fuel populism. Carmakers,

clearly are next. (our note) ‘It’s going to be the biggest change we’ve

seen in the last 100 years and it’s going to be really expensive even for the

biggest companies,’”…The major auto companies will spend well over $400 billion

during the next five years, developing electric cars equipped with technology

that automates much of the task of driving…”

↓ We Also Suggest ↓

7/1/19

–

On

6/21/19 the S&P 500 closed at 2953, close to an all-time high. The

following are the return premiums that were available on the date in the U.S.

financial markets.

2.50% Fed Funds

-.31% 10 Year Treasury Premium

2.35% BAA Corporate Bond Premium

.49% S&P 500 Premium

5.03% Return of the S&P 500

The

10 year treasury bond rate of 2.19% is extraordinarily

low and below the Fed funds rate. The S&P 500 return of 5.03% says that the

risk of the S&P 500 is only slightly above that of the average corporate bond’s. Clearly, the financial

markets do not expect a future of high economic growth over the long-term.

The

financial market have, very likely, not factored in

global warming, which should raise interest rates along with sea levels. What

they currently expect is a likely future of low growth for the following

reasons:

1)

Both

the U.S. and Europe (for structural reasons) are unable to effect fiscal

policy. This illustrates that the private sector, alone, cannot lift economic

growth without an active role of government; and justifies Keynes’ invention of

macroeconomics..

2)

Continued

demographic problems in Japan.

All

three economies together are responsible for 52.1% of world GDP (World Bank,

2018), now add the Administration’s trade and foreign wars…

These

available rates surely do not justify long-term portfolio investment; and for

shorter-term investors, the returns do not justify the risk, granting Mr.

Market’s disregard of the fundamentals.

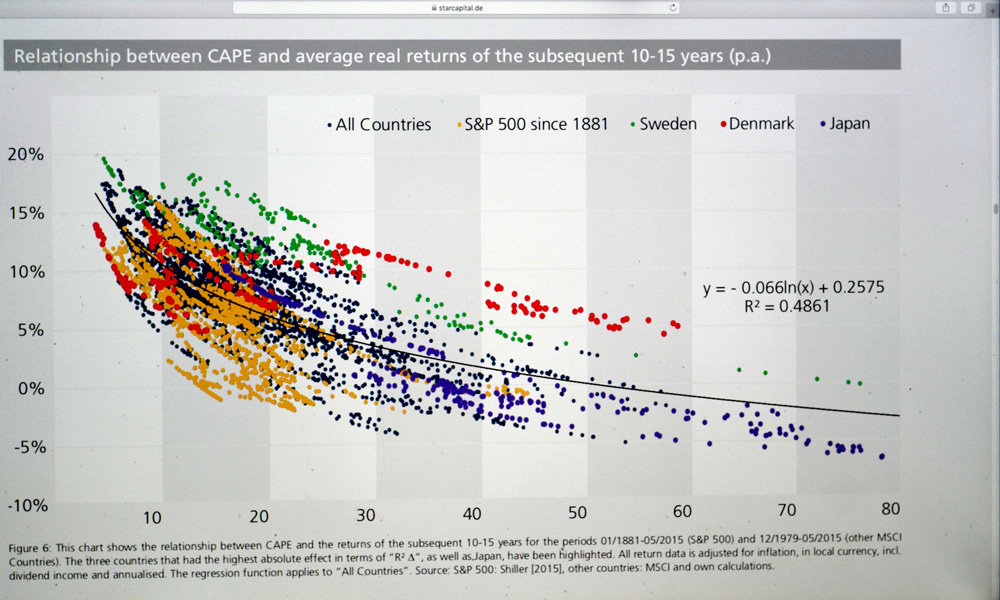

According

to a Star Capital, a German value money manager, on 4/30/19 the U.S. stock

market had almost

the world’s highest Schiller CAPE

(Current Price/10 year earnings average) ratio, which adjusts for cyclicality. That

value was 30.6 in the U.S. By comparison, Germany’s CAPE was 18.8, even though

the yield to maturity of the ten year Bund was only

.013%, equivalent to zero. Their graph,

for major markets, illustrates the relationship between CAPE and subsequent

real 10-15 year returns. The R2 coefficient

of this analysis is only .4861 *, but the direction of this analysis should be

very clear. In financial markets, a high CAPE leads to low future returns. This

is without discussing the additional effects of historically low interest

rates, that should increase.

{kind=link}

*A

correlation of .6 is considered adequate for social science studies. In our

experience, a correlation of greater than .95 is necessary for an exact

empirical market level statement (which is rarely possible).

↓ We

Also Suggest ↓

8/1/19

–

On

7/26/19 the S&P 500 closed at 3026, yielding long term investors a return

of only 4.90%.

To

illustrate the problems that this might cause, assuming the goal is to

structure a portfolio whose income will last for decades, a portfolio split

50/50 between a S&P 500 index fund and 10 year

treasuries would yield a likely inflation-proofed income return of only 1.88%.

The 3.4% long-term rate of return of this portfolio should be compared with an

assumed rate of return of around 7.45% (NASRA, 2018) for pension fund

portfolios, which is another problem.

This

is the result of the central banks’ determination to boost stubbornly slow

economic growth by drastically lowering interest rates, relying only on the

private sector to sustain growth. According to the 7/27/19 Bloomberg,

European Central Bank President, Mario Draghi, recently complained that

monetary policy has borne a “disproportionate” burden in recent years. But,

until fiscal policy becomes politically possible (for the government to combat

global warming, rebuild U.S.’ D+ grade infrastructure and remedy income

disparities), the burden will remain on monetary policy to maintain economic

growth. This burden will become increasingly difficult given:

·

Continued

Trade Wars and Foreign Crises.

·

Low

growth caused by demographic changes and a reduced supply of skilled labor,

resulting in a decreased natural rate of interest.

·

The

Diminishing Effects of Tax Cuts, (Leaving $1 trillion deficits as far as the

eye can see.)

Decreasing

interest rates might be a present value argument for stocks remaining high. But

considering the above, something could easily happen to affect perceptions

about the future. There has to be some change to avert the continued

deterioration of our political-economic system. We hope that change will occur

in the 2020 elections, because the present (“Divide and Conquer”)

Administration has no ability to get the social cooperation necessary to deal

with looming, large scale problems.

)

__

A

journalist once wrote that the election of Donald Trump would make Americans,

“sicker, dirtier and poorer.” (We can’t find the reference to this memorable

quote on the Internet.) Almost three years into his term, the President has

accomplished the first two:

·

Due

to the GOP inability to “repeal and replace,” 7 million fewer Americans are now

covered by healthcare insurance (Gallup, 1/19 poll).

·

Carbon

emissions continue to grow, causing the five warmest years in modern record.

(NASA)

Now,

with his, “Trade wars are good and easy to win,” Donald Trump risks plunging

the world into a recession. By imposing blanket tariffs on China, costing each

American family an estimated $725/year (NYT, 8/6/19, calculation $92.5 billion

additional tariffs/127.59 million households). He is well on his way to making

Americans:

·

Poorer.

A 8/7/19 CNN headline reports,

“Stock sink as rates fall.” This unconventional behavior is caused by the

market expectation that a world-wide recession will be on its way. But, Trump

economic advisor, Larry Kudlow notes, “The Chinese economy is crumbling under

the weight of tariffs.” They can bear less pain than us? He neglected to note

the cost of the Trump tariffs to the American family and the cost of forcing

vulnerable family farms out of business in the Midwest.

History

is full of unforced errors, that is not doing the right and rational thing,

thereby contradicting reality and truth. In 2016, an emotional electorate chose

a fearful leader who could lead the nation and the world off a cliff. We hope

they don’t make the same mistake in 2020, their discontents exacerbated by the

very same leader they chose.

__

There

are no guarantees that a social order will be able to successfully meet the

challenges it faces. In 1933 during the Great Depression, Keynes wrote, “I feel

that general disaster for a great country like United States is a far more

unlikely event than disaster for particular firms or industries, and that nine

times out of ten it is a safe bet that the extremes of misfortune will not

occur. (Investment and Editorial)." FDR was then president, giving

the nation hope. We question whether the present Administration can at all lead

the U.S. and the world to meet the acute challenge of climate change.

David

Archer is a professor in Geophysical Sciences at the University of Chicago. In The

Long Thaw (2009) he writes, “Climate change is a global issue that ramps up

slowly and lasts for a long time. Negotiating a solution would require a degree

of global cooperation that is I think unprecedented in human history…The

situation looks a little more daunting, however, when viewed in the global

scale over the coming decades. CO2 emission is closely tied to

economic and military supremacy (i.e. money and power) in our world.”

The

first problem is that “Money flows toward short-term gain, and toward

over-exploitation of unregulated common resources.…Our understanding of

economics tells us that the free hand of the market, also known as

business-as-usual, will not cope gracefully with the threat of global warming,”

without the policy of governments. When it comes to the long-term, the

invisible hand fumbles badly.

The second problem is how policy is made

in Washington, with the ability of the fossil fuel industry to bend government

environmental and energy policy to their interests with money and untruths. The

latter is an example of why the truth really matters; because untruth will lead

the whole world to maladaption and disaster. As a climate author notes, we burn

failed species in our car every day.

The

2020 U.S. elections will likely be the last chance to limit the consequences of

extreme global warming.

9/1/19

–

On

8/23/19 the S&P 500 dropped another 2.59% in one day to 2847. In response

to prior U.S. tariffs, China announced retaliatory tariffs on another $70

billion in imports from the U.S., in addition to imposing a 25% tariff on U.S.

auto imports. President Trump then tweeted, “We don’t need China and, frankly,

would be far better off without them.” He also “ordered” American companies,

“to immediately start looking for an alternative to China.” He then boosted

tariffs on existing Chinese goods another 5%. An effective effort would have

been to put together a coalition of nations, to remedy specific trade complaints.

This could have been the traditional exercise of American power for the greater

good, the reason the world did not oppose American leadership in the past.

__

This

tariff war has the potential to bring what Harvard Professor Larry Summers

called, “secular stagnation” to the whole world. On the same day he said on

CNBC, “We’re one recession away from zero interest rates.”

In

2016, the American electorate chose a clueless, divisive and fearful leader to

“shake things up,” who is now leading the world off a cliff. In “On the Origins

of War,” the historian Donald Kagan (1995) wrote that the unraveling of the

international system led to the carnage of the two world wars (this unraveling

is already starting in parts of the Mideast and Asia as regional animosities

reassert themselves).

“…Henry

Kissinger suggests (in the 19th century) international stability

was, ‘so pervasive that it might have contributed to disaster. For in the long

interval of peace the sense of the tragic was lost, it was forgotten that

states could die, that upheavals could be irretrievable, that fear could

become the means of social cohesion.’ (our note)…

“A

pertinent and repeated error through the ages has been the failure to

understand that the preservation of peace requires active effort, planning, and

expenditure of resources and sacrifice, just as war does….If their successors

forgot these things the practical men of affairs who managed Europe’s international

system in the years after 1815 68.7 atmospheres). did not. They knew that peace

does not keep itself, that one or more states in any international (or

financial) system must take the responsibility and bear the burdens (and pay

the price) needed to keep the peace, so they established an international order

meant to last, and they were prepared to defend it.”

What ultimately undermined this order was,

“the searing power of nationalism,” * motivated by the angst of the

dislocations caused by the growth of capitalism. History is beginning to repeat

itself.

*

Quotes; Donald Kagan; “On the Origins of War”; Random House, Inc.; New York,

N.Y.; 1996 (ed.); p. 567.

10/1/19

–

The

international oil market is currently well supplied. But an eighteen drone *

attack on Saudi Arabia’s Abqaiq oil processing facility and a major oil field

has taken out 5.7 mm barrels/day, over half of the country’s daily oil

production. On 9/16/19 Brent crude increased to $68.02, up 12.9% for the day.

The S&P 500 dipped only slightly by -.31% to 2998.

The

impact of this attack on the oil market will depend upon whether Abqaiq can be

fully repaired in weeks or months. We think the repairs will take months. The

Abqaiq oil processing plant desulfurizes and separates oil from gas. ** Aerial

reconnaissance shows extensive damage:

1)

The

drone strikes precisely targeted

the plant’s spheroid oil and gas separators. They did not just aim at a few oil

storage tanks.

{kind=link}

2)

They

damaged or destroyed half the desulfurization towers.

The

oil and gas separators operate at medium pressure (up to 100 psi or 6.8

atmospheres). The desulfurization towers likely run the HDS process, which is

both high temperature and high pressure. These units are not available

off-the-shelf; they must be precisely rebuilt. According to the 9/16/19 FT,

“Analysts say it could take months to fix damage at Abqaiq…”

*

These drones are built from off-the-shelf parts. The 9/15/19 MIT Technology

Review reports that they cost no more than $15,000 each.

**

Reprocessing is also one of the businesses of the domestic oil pipelines.

_

We

learned in accounting to ask the question, “What is reality?” What’s happening?

This

is what’s happening in Saudi Arabia. 1+1 has to equal 2, in the long-run.

_

The

9/23/19 United Nations Climate Action Summit was a bit of a disappointment. Roughly

60 countries announced efforts to achieve net zero emissions by 2050; but for

the near-term, the United States did not even apply to speak, China did not

signal its readiness to issue stronger targets than the 2015 Paris Agreement,

The European Union did not intend to cut emissions faster either and India did

not promise to reduce its dependence on coal. The following figure projects the

total existing energy infrastructure's CO2 emissions. Between 2018 and 2059

the U.S. will add 57 gigatons of CO2 from existing infrastructure,

China will add 270 and the rest of the world will add 330. (This is a graph

from the Tong, Zhang, Zheng and Caldeira (2019) study

we earlier cited in “The Dimensions of Climate Change.”)

But,

country population considerations aside, we’re all in the same boat.

Why

this inaction in the face of increasingly dire climate prognoses? A 2019 United

Nations climate synthesis report notes:

·

The

average global temperature for 2015-2019 will be the warmest of any equivalent

period on record. It is currently estimated to be 1.1 °C above pre-industrial

times and 0.2 °C warmer than in the previous five years. Assuming no

acceleration in global warming, the average global temperature will likely

exceed the critical 1.5 °C level by 2029 – just a few years off.

·

Due

to the increased heating of the oceans and the melting polar ice, the global

sea-level rise increased from 3.04 millimeters/yr in

1997-2006 to approximately 4mm/yr during the period

2007-2016. Assuming no acceleration in sea level rise, by 2100 this level will

increase by 3.36 meters, or 11 feet. (The average level of Miami is 6.5 feet,

the average level of Antwerp -a major port- is 16 feet).

·

Heatwaves

were the deadliest weather hazard in the 2015-2019 period, affecting all

continents. In 2019, heat waves killed 1.435 people in France alone.

·

Increased

rainfall and higher temperatures favor vector-borne diseases, such as

parasites, viruses, and bacteria transmitted by mosquitoes (carrying EEE),

ticks and fleas.

In

the face of increasing climate adversities, why don’t people do something? In

1968, biologist Garrett Hardin wrote an article, “The Tragedy of the Commons.”

As the Wikipedia summarizes, “ The tragedy of the commons is a situation

in a shared resource system where individual users acting independently

according to their own self-interest, behave contrary to the common goal of all

users, by depleting or spoiling that resource through their collective

action…Although common resource systems have been known to collapse due to

overuse (such as over-fishing), many examples have existed and still do exist

where members of a community with access to a common resource co-operate or

regulate to exploit those resources prudently without collapse.” 1

Put

very simply, since the planet’s annual CO2 production exceeds its CO2

absorption capacity by much more than 50%, the problem of global warming will

therefore get more acute. 2 What kind of social system and economic

system is most appropriate for the U.S., a mixed system which emphasizes “Home

on the Range” freedoms or a mixed system which emphasizes one’s responsibility

to others as still exists in the communal town-hall meetings of New England?

The consequence of the first kind of social system is vastly accelerated global

warming. The consequence of the second kind is the possibility that global

warming can be slowed, also with the aid of science and technology.

To

deal with the large problem of international global warming, the United States

must first credibly deal with its own CO2 emissions. In that

process, it also has the opportunity to develop major renewable energy

industries.

1 There is also the

structural problem of entrenched interest, which we shall discuss in a later

article.

2 Professor Richard Betts is

a head researcher at Britain’s Met Office, which deals with climate research.

In Carbon Brief article,

he notes the average annual Sources and Sinks of the world’s CO2

emissions between 2005-2014.

Gigatons

CO2/Yr

Fossil

Fuels and Industry 33.0

Land

Use Changes 3.4

-Land

Absorption -10.9

-Ocean

Absorption - 9.5

Yearly Atmospheric Change +16.0 = Increased

Global Warming

11/1/19

–

On

10/18/19 the S&P 500 closed at 2986, yielding an investment return of 5.1%.

The following compares the asset return premia available on that date with

those available on 1/18/19 and with the normal case.

Condition

Condition

Normal Conditions 1/18/19 10/18/19

2.5%

Policy rate

2.5% 2.0%

2.0% 10

year treasury premium .4% -.1%

2.0% Corporate

bond premium 2.4% 2.2%

2.0% Equity risk premium 0% 1.0%

8.5% Normal equity return 5.3% 5.1%

The

Fed’s policy rate has declined from 1/18/19 to lower the risk of a recession.

Interpreting the change in market spreads, the ten year

bond curve has flattened, signaling a possible recession. The corporate bond

risk premium has remained high. The equity risk premium has increased.

1)

Taken

as a whole, the financial markets signal increasing risk.

2)

The

low expected return of long-term financial investments does not compensate

investors for risk.

__

In

an interview on 60 Minutes, the new European Central Bank president,

Christine Lagarde noted:

1)

The

greatest worldwide uncertainty is to (the system of international trade). You

can’t adjust to the unknown. So what do you do? You

build buffers; you build savings; you wonder what comes next. That’s not

propitious to economic development. Interviewer: People stop taking

risks? Yes, they sit on their cash.

2)

If

things go wrong in one part of the world, its going

to affect the rest of the world as well.

3)

Some

Americans say, ‘…what do I care?’ Because of the interconnections, next door is

not down the pathway. Next door is everywhere in the world, and if my neighbors

from across the border are feeling desperate and starving and fighting, there

will be consequences back at home.

4)

The

risk, I feel, is that the United States is at the risk of losing leadership and

that would be just a terrible development because the U.S. has been a force for

good and for the principles that I respect highly: The rule of law, democracy,

free markets, consideration for the individual and respect. Interviewer:

We’re all in this together.

These

observations also relate to the concerted action required to deal with global

warming. If the U.S. is going to resume its necessary leadership role in the

world, it must be able to give hope to those in its own rural communities.

__

To

give our country hope, it will first be necessary to change a president and his

administration in Washington. A political science professor says changing

voters’ minds and values are a long-term strategy. In the short term, “Outorganize

and Vote!”

__

What is U.S. foreign policy all about? On 10/11/19

(Republican) Ambassador William B. Taylor testified to the House impeachment

investigation on Ukraine:

“Ukraine is important to the security of the United

States. It has been attacked by Russia, which continues its aggression against

Ukraine….

“There are two Ukraine stories today. The first is

the one we are discussing this morning and that you have been hearing for the

past two weeks. It is a rancorous story about whistleblowers, Mr. Giuliani,

side channels, quid pro quos, corruption and (sought) interference in (U.S.)

elections. In this story Ukraine is an object….

“But there is another Ukraine story -

a positive bipartisan one. In this second story, Ukraine is the subject.

This one is about young people in a young nation, struggling to break free of

its past, hopeful that their new government will finally usher in a new

Ukraine, proud of its independence from Russia, eOn

ager to join Western institutions and enjoy a more secure and prosperous life.

This story describes a nation developing an inclusive, democratic nationalism,

not unlike what we in America, in our best moments, feel about our diverse

country….”

We are lucky that there are so many people in the

government who are dedicated to the service of this nation.

12/1/19 –

On 11/26/19 the S&P 500 closed at 3141,

essentially a record high, yielding a 4.85% return to long-term investors. The

reason for this was a series of cuts in the Fed’s policy rate (a), that lowered

the required rate of return from equities (b), resulting in a large S&P 500

short-term capital appreciation of 17.6% between 1/18/19 and the present. This

is good news for short-term traders, but bad news for long-term investors, who

will experience very low rates of future returns.

Condition Condition Condition

1/18/19 10/18/19 11/26/19

Policy rate (a)

2.5% 2.0% 1.75%

10 year

treasury premium .4% -.1% .19%

Corporate bond premium 2.4% 2.2% 2.11%

Equity risk premium 0% 1.0% .80%

Equity return (b) 5.3% 5.1% 4.85%

If the Fed were willing to lower interest rates

indefinitely, we could construct an argument that stocks will appreciate

indefinitely; but, as the Wall Street saying goes, “Trees don’t grow to the

sky.” The market is assuming that a perpetual lowering of interest rates will

lower the discount rate and furthermore make additional projects feasible,

causing additional investment and thus economic growth. The latter hasn’t

happened (but the treasury bond yield curve has turned slightly positive). A

11/19/19 WSJ article

notes, “…weak economic growth made new factories unappealing, while the

disruptive technologies where investors wanted to spend their money didn’t involve

much investment….Shareholders rightly worried about the economy as it bumped

along at the slowest average growth in more than half a century…”

The Atlanta Fed estimates that fourth quarter

economic growth will be 1.7%; the Conference Board’s leading indicators have

grown by only .3%; and there has been a year-over-year 5% drop in job openings.

Manufacturing is already in recession. Economic growth in the EU and Japan is

very low. The major problems of the world economy are structural, depressing growth,

rather than cyclical.

Since it’s holiday season, we won’t

continue with this; but do read our new article and enjoy the holidays. Add:

But the impeachment of President Trump necessitates the following:

__

The

democratic political order guarantees our rights and freedoms. This order is

threatened by the betrayal of the national interest and by corruption; we see a

glimmer of something much worse.

At

the end of W.W. II, the political philosopher Hannah Arendt wrote, “The Origins

of Totalitarianism,” likely the defining work that described the deterioration

of all traditional political orders and the rise of their substitute. Before

the Enlightenment of the 17th century, the most common form of

government was loosely authoritarian. What enabled Nazi and Communist

totalitarianisms were economic globalization and the technological developments

of the radio and the railroads, providing authoritarian leaders with the

opportunities and means to extend their rule over a now atomized mass of

people. In the 21st century, the Internet and hyper-globalization

provide authoritarian leaders with the same situation, enabling them to harness

angry passions to extend their rule, again placing the balanced liberal

democratic system of shared power at risk.

Read

how Professor Arendt described the totalitarian system. This may begin to sound

familiar to our readers in the United States. “Without the elite and its

artificially induced inability to understand facts as facts, to distinguish

between truth and falsehood, the movement could never move in the direction of

realizing its fiction. * The outstanding negative quality of the totalitarian

elite is that it never stops to think about the world as it really is and never

compares lies with reality. It most cherished virtue, correspondingly, is

loyalty to the Leader, who, like a talisman, assures the ultimate victory of

lie and fiction over truth and reality.” ** In other words, with their powers,

the totalitarian leader and his followers live in and try to construct a dream

world.

We

hope this makes Americans uncomfortable. Are a few quarters of low interest

rate induced economic growth (initial economic growth also occurred in Nazi

Germany and in Russia) worth giving up our system of government? Our

revolutionary conservatives must also ask whether their ideology offers any

real solutions to the increasingly acute problems of economic inequality,

social stability and climate change. What is happening is national weakness

abroad and a corruption of the Presidency.

*The

goal of Communism was an unworkable communal ownership of the means of

production. The goal of Nazism was the world-wide domination of a predatory

elite. In the U.S. and U.K., the goal is a restoration of past national glory,

in contradiction to the reality of an highly

interdependent economic order. (What this suggests is that the first goal of

political life is security; and people seek various means, both foul and fair –

effective and ineffective, to get it.) In business, Steve Jobs’ “reality warp”

can result in new products and services. In politics, this is very dangerous

because it leads to impatient behavior and much worse.

The

sentence in parenthesis is purposely ambiguous; because these are the kinds of

alternatives that the world can present. Isaiah Berlin wrote, “values

conflict.” But what matters the most, and we note this is especially true in

the long run, is the choice of value(s) that one makes. From that,

hopefully sound, initial choice flow - to get technical – subsidiary positive

correlations. These have practical consequences that we will explore in our

next economics essay.

**

Hannah Arendt; “The Origins of Totalitarianism”; 1951.