1/21/22 - NOTES

We sold our

pharmaceutical manufacturer (GILD). As usual, we highly recommend that you

discuss any portfolio trades with your qualified investment advisor. As a result

of this sale, our portfolio has less than 20% equities, with the remainder held

in money market funds.

We are, of

course, considering how our portfolio should look when financial values become

more favorable. A traditional benchmark is that the proportion of bonds in a

portfolio should be equal to your age. This, however, assumes that bond returns

exceed the rates of general inflation. This is presently not the case, and will also likely not be the future case. This

means that a portfolio should probably be biased towards equities contain

a greater proportion of equities, for both income and growth, with the

portfolio necessarily bearing a greater duration (interest sensitivity) risk.

Should this be

interpreted as having an all-equity portfolio? Definitely not; but equities representing real assets, do eventually

provide a hedge against inflation.

__

As mentioned

above, a flattening yield curve means a lesser amount of short-term capital

loss. The 1/31/22 Barron’s indicates that this is already

occurring. “The yield curve is flattening quickly. (On Friday the gap between

the two year and ten year treasuries was

.61%. On December 31, the gap was 1.069%.)…Recessions

usually follow in eight to 19 months….David Rosenberg…expects the Fed to lift

rates aggressively, only to find that the economy is growing at a much slower

pace than it thinks.” The U.S. economy is not the highly cyclical and

industrialized one of the past.

We think our

markup model (extended to the S&P 500, add: a widely

traded asset) is the best way to determine whether or not

to invest. But, is it natural law? In the physical

sciences, there are several physical laws that anchor entire disciplines (the

simplest is F=ma and it gets much more complicated). In finance, the law,

formulated amongst “Manias, Panics and Crashes” is: “Do you want to eat well

(return) or sleep well (minimize risk).” More seriously, the key question in

finance is “What do you REASONABLY want?” We could, for instance, consider a

10% (incl. inflation) rate of return for the S&P 500, “reasonable”. A

well-chosen historical study of years 19XX-20XX could assert that the stock

market return in those years, in addition, constitute “natural law.” Not so,

that return is contingent upon a raft of contingent what ifs that had become

actuality.

If you look at

current markets (and our S&P 500 present value model), you will see the

following:

1/28/22

Reasonable

Returns Current

Returns

Policy Rate 0%-2% .08%

10

year treasury

premium

2%-0% 1.70%

BAA

corporate bond premium 3% 1.91%

Equity

risk

premium 1% .18%

Equity return 6% 3.87% S&P=4331

Considering

simpler BAA rates over

a ten year period, we think to wait for an adequate S&P 500

equity return is very reasonable; income-earning assets have been very

overpriced. But, if you can find a low-risk opportunity, after asking why God

has given this to you (Greenwald in class), why not take it? The above also clearly

illustrates that the financial markets do not make opportunities available at

the same time. In this case, reasonable equity returns will probably be

available before BAA bond returns, which are very low indeed.

__

Does President Putin want empire or more security? Most likely he

wants more security and would try to grasp for empire only if its additional

costs were minimal. (We hope.)

2/17/22 -

We have demonstrated that long-term stock returns depend upon stock yields (1.33 X the 10 year average of S&P 500 operating earnings per share/the current level of the S&P 500) and (considering incremental equity risk) the bond yield curve. With the above, we can now discuss portfolio structure. We encourage you to talk with a qualified investment advisor about this.

For a portfolio to last for many years, you have to live within its income – both from stocks and bonds. This is the reason why, with an exception below, we have been waiting for interest rates (rates of return) to increase. The problem with markets greatly exceeding fair valuation is this: after years of overvaluation relative to some Fed long-term equilibrium interest rate (like 2%+), what do you now do without crashing the market? Better the U.S. economy, as in the past, had operated on shorter cycles; the conventional wisdom that one should always continue to invest would have made better sense.

Markets are subject to “Manias, Panics and Crashes.” Here is what our portfolio will likely do relative to various levels of inflation:

Level/Asset Money Market Gold Stock A Specific Utility

High Inflation + + (moderately -)

Medium Inflation 0 0 +

Low Inflation 0 0 +

Wars and their collateral damages surely create high inflation; but so do plagues, because both restrict supply.

John Maynard Keynes was also an accomplished investor. Setting investment policy for his alma mater, King’s College, Cambridge in 1938, he wrote, “…successful investment depends on three principles:-

(1) a careful selection of a few investments (or a few types of investment) having regard to their cheapness in relation to their probable actual and potential intrinsic value1 over a period of years ahead, and in relation to alternative investments at the time.

(2) a steadfast holding of these in fairly large units through thick and thin2 perhaps for several years, until they have fulfilled their promise or it is evident that they were purchased on a mistake.

(3) a balanced investment position, i.e. a variety of risks in spite of individual holdings being large, and if possible opposed risks (e.g. a holding of gold shares amongst other equities, since they are likely to move in opposite directions when there are general fluctuations).”3

1 Although stocks are very traded, they really do have intrinsic value. In Keynes’ time, a company’s intrinsic value was determined mainly by its book value on the balance sheet. Now, it is determined by a company’s likely net cash flow, on its cash flow statement. Keynes was one of the first value investors.

2Being a stock investor requires a consistent investment philosophy, if you are always in touch with the markets. For most people, the best attitude is simply to ignore the market until the price is not prohibitive and then invest steadily.

3During Keynes’ time, individual stock holdings were much more prevalent than mutual funds. Diversification is much easier with mutual funds. Also, as John Bogle of Vanguard contended, the long-term minimization of cost is key.

To determine the appropriate cash flows discount rate, the Capital Asset Pricing Model used by modern finance is sort of like a very general Swiss army knife, very flexible; but is basically a financial equilibrium model, also too dependent upon chosen market history. A current and likely bond yield curve model is more appropriate, obviously for bonds, but also for stocks as well.

J.M. Keynes;

“Economic Articles and Correspondence, Investment and Editorial”; Macmillan

Cambridge University Press; London; 1983; p.p. 106-107.

__

In poker terms, President Putin is, “Going All In.” A 2/16/22 WSJ article now states his likely goal:

“In massing troops near Ukraine, Mr. Putin’s goal is to extract (significant) concessions from Ukrainian President Volodymyr Zelensky and force him to give Russia a say in Ukraine’s future. That would send a message to other former Soviet states that the West can’t guarantee their security. To ratchet up the pressure, Mr. Putin has an array of military options short of a full occupation, from low-profile incursions to a limited conflict in the eastern Donbas region, where Russian-backed separatists have declared themselves independent of Ukraine but aren’t recognized by the government in Kyiv.”

The world’s post W.W. II political regime of independent nation states governed by the rule of law is being challenged by the power of, well, power. The slogan of, “Make Russia Great Again” will result in a highly insecure world – the world as it was in the late 19th century. If there is a war, we see all downside for Russia and great problems for the world.

There is a further problem. Wars have a way of spiraling and are therefore irrational because their consequences can’t be determined in advance. In spite of reassurances, the outcomes of war are highly unpredictable. To cite just two examples: The Peloponnesian War started with an attack on a small city-state; it ended almost three decades later with the entire Greek civilization fatally weakened. The two World Wars started with the reassurances on all sides that they would be home by Christmas, 1914. The wars ended with the fall of empires and the rise of the nation-state in 1945.

__

On 2/24/22, detached from reality and acting out to fear, President Putin has attacked Ukraine. Detached from reality, Donald Trump called Putin’s aggression “very savvy,” and a “genius” move. Should either be President?

__

This is a website of political economy. The two can be normally considered separately. The first addresses the fundamental bases of market societies, and the second the practical bases of, “keeping the shop open.” The first is normally taken for granted; but during times of conflict with (traditional) authoritarian societies or (non-traditional) totalitarianism a clear choice must be made. This statement by former Ukrainian President Petro (Peter) Poroshenko says it all.

Ukraine is now in what the Germans call a grenzsituation, an extreme condition; and given the popular will is likely to win; but in the long-run.

5/18/22 –

It would seem quite logical that investors would demand a higher return from riskier assets. Now, we can place all major financial assets along a continuum of risk and return, by combining a qualitative (ordinal) measure of risk with a quantitative measure of available market returns. We compare a logical expectation on 5/21/21 with the actual financial market, one year later, on 5/10/22:

Logical Expectation 5/21/21 Actual Market 5/10/22

0% Policy Rate

.83%

2% 10 year treasury premium 2.22%

3% BAA corporate bond premium 2.17%

1% Equity risk premium (.75)%

6% Equity return

4.47%*

*St. Louis Fed FRED data, calculation of S&P 500 returns at the 4001level.

The financial markets do reflect an approximate truth, because the first three rates sum up to a total expectation of around 5%. But, real financial markets are also affected by the supply and demand conditions in each individual market, and the simple economic equilibrium that economists assume is disturbed by other practical factors like: 1) Fed policy 2) Foreign wars 3) Snarled supply chains 4) Past practice.

Mohamed El-Erian, senior advisor to Allianz, says in the 5/6/22 Bloomberg, “…we have mostly priced in interest rate risk. We haven’t priced liquidity risk, we haven’t priced credit risk, we haven’t priced (market) functioning risk. We are still in the process of pricing it. The days of abundant and predictable liquidity are gone.”

As a result of all the above, we think it is justifiable to increase our target rate of our equity returns from 6% to 6-7%. The 7% target would reflect the assumptions we were making before the 2008-2009 crisis, but not before the inflation-prone economy of the last half of the twentieth century, described by Jeremy Grantham. We could further cite: climate change, the adverse demographics of the global work force and globalization itself unsettled. But what happens depends upon what people do. This is, after all, the Anthropocene era. In the face of these challenges, it is only possible to make an investment decision that a specific return is both practical and adequate for the times (we hope).

__

We have been showing that real markets are subject to, “events” and are therefore not mathematically well-behaved. Market economics is not physics.

Generally speaking, if you have the temperament of trader you will look at short-term events affecting the market. If you have the temperament of an investor, you will look at long-term earnings growth, hopefully anchored inflation expectations, climate change and so on.

Amid fluctuating markets, it is necessary to focus on the basics:

1) The rule of law, guaranteeing, at a minimum, property rights; also the rule of common sense.

2) For those primarily interested in other things besides markets, a continued series of small investments is appropriate, if the market has a decent rate of return (which is around 90% of the time, our estimate *).

3) For those very interested in markets (as we are), having an investment philosophy is crucial. To manage complexity, it is really important to have a philosophy. The two major investment philosophies are value (as measured by a long-term increasing return on investment) and momentum (as measured by a long-term decreasing return on investment). You obviously can’t do both well. If you are interested in markets, search your soul, and then become proficient at one or another.

4) If there is anything that makes one tolerant of differences, its markets. **

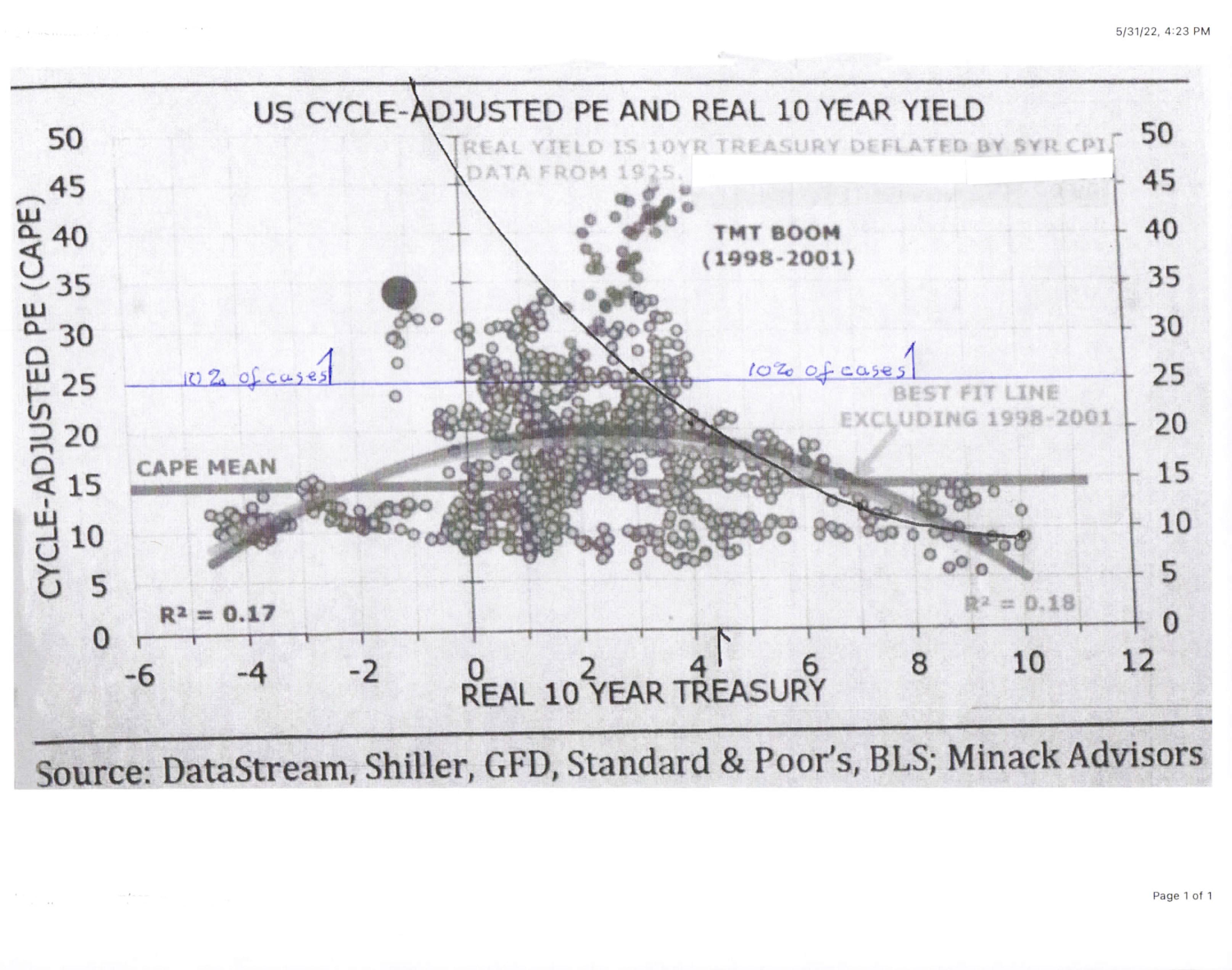

* This 12/20 graph from Minack Advisors is really useful because it shows that inflation, i.e. negative real rates, is eventually subdued by the Fed resulting in positive real interest rates. For our purpose, it also shows that 10% of the time, i.e. in around 114/1140 cases, the market is likely to produce low returns because the CAPE P/E is over 25, 156% of the average CAPE level of around 15. (We can now easily translate a CAPE P/E of 25 into a long-term rate of investment return: (E/P=1/25) x 1.33 = 5.32%, too low for equity). The Minack analysis assumes higher levels of interest rates, comparable to historic levels, in the future.

{kind=link}

** And markets can often chew gum and walk straight at the same time (an Americanism) because they have participants with different goals and viewpoints.

This assumes a common basis of trust, a very interesting discussion that ought to be held more often, surely within and also across societies. There are now a common set of challenges confronting all.

__

Logical Expectation 6/16/22 Actual Market 6/16/22

2% Policy Rate

1.58%

2% 10

year treasury premium 1.70%

2% BAA

corporate bond premium 2.13%

1% Equity risk premium (S&P 500=3666) (.53%)

7% 4.88%

Valuation, to see things at their worth, is the core concept of finance, the concept discussed in finance textbooks. However, the day-to-day behavior of the financial markets is another thing; because it is like life itself - highly context dependent. What most matters is who is doing what, in response to market price as it affects supply and demand.

Concerning large portfolio changes (in response to now unavoidable interest rate increases, after more than a decade of repression by the central banks), the “who” that really matters is the Open Market Committee of the U.S. Federal Reserve, as it struggles to contain increasing inflationary expectation. Note the 4/22 increase in add: 12 month hence inflationary expectation to 5.4% relative to a historic long-term Fed goal of 2% inflation.

,

According to Milton Friedman, “Inflation is always and everywhere a monetary phenomenon…” But the reverse is not necessarily true, because a large shift in monetary regime also occurred after 2012 (The Fed response, to keep the economy going after 2009), even during the Trump years (to keep shareholders happy), to combating the depressing effects of the COVID Plague (to keep everyone going) – inflation expectations remained relatively subdued until 3/21; and then Putin decided to invade Ukraine on 2/22. This caused another large economic regime shift towards supply shortages. Since the beginning of 2022, wheat has gone up by 36% and the weighted cost of crude oil has gone up by 42%. And, as the Michigan survey indicates, high inflation is now becoming embedded in people’s expectations, causing the Fed a large problem.

The problem facing the Fed, and as a World Bank study also indicates (we find the checked paragraphs highly relevant), is that circumstances are unprecedented: 1) The response of world economies to higher interest rates is unknown (but something has to be done) 2) The problem of manufacturing supply chain snarls in China can’t be remedied by monetary policy 3) The Ukraine war continues. *

Increased interest rates are the tool the Fed has to depress demand. But there is considerable uncertainty as to their effects. Too high interest rates will cause a recession. Too low interest rates will have no effect on inflation. What is just right? In complexity, is there a “just right?” Perhaps there is no automatic mean reversion to equilibrium (as is characteristic of Gaussian risk formally defined), but economic error-correction in the face of uncertainty, with long-term mean behavior a Fed goal. We refer to our original observation, which describes the error-correcting process.

It is with this backdrop that we are challenged to come up with an appropriate portfolio policy. Due to the above large uncertainties; we will, for sure, spread out our increased exposure to a medium-term corporate bond ETF over time. Our goal is to achieve a 50/50 bond-equity portfolio. We have now started increasing our bond exposure, in 10% of the entire portfolio increments. Should the increments be 10% approximately every month or in two months? Our sense is this interest rate cycle will be prolonged before demand decreases convincingly. However, neither we or the Fed are sure of this. Fed policy is “conditions based,” deciding interest rate policy meeting-by-meeting. We’re suspending judgment as to time period until we get more information that includes Fed policy.

As for U.S. equities, they are still too high.

*A 6/17/22 Washington Post article clarifies the stakes for all involved in Ukraine, which through now constrained markets is everyone:

“Kyiv and its backers can hope for little more than a stalemate with Russia’s far bigger, better armed military….’That would mean feeding Ukraine to the wolves,’ Daalder said, referring to a withdrawal of support. ‘And no one is prepared to do that.’”

At this point, a past U.S. president with a too “narrow (moi) perspective, even for business, would likely say, “Settle for what you can get, retreat behind our borders, MAGA!” add: An excellent article in the July/August 2022 Foreign Affairs titled “The Perils of Pessimism” notes that, “Foreign policy elites cope with…uncertainty by fashioning coherent narratives about whether the future is favorable or unfavorable to their country’s interests. Ideologies such as Marxism and liberal internationalism, for instance, rest on visions of progress based on certain actors inexorably rising to power and prosperity. More pessimistic narratives include historical cycles of rising or falling or of terminal decline, violence, and rebirth.” Do you think that Donald Trump is an optimist or a pessimist? Do you want him to lead you again? How do you rate Putin? We note this because, the exact applies to stock market investors. You have to be optimistic to be an equity investor (at least around 89% of the time).

We don’t like to note this. But, “…officials have

described the stakes of ensuring Russia cannot swallow up Ukraine – an outcome

officials believe could embolden Putin to invade other neighbors or even strike

out at NATO members – as so high that the administration is willing to

countenance even a global recession and mounting hunger.” 1 The Ukraine crisis is where a

qualified and broad foreign policy experience really counts. Getting out of

this crisis in Europe is going to take a lot of skill, as this conflict is

evolving into stalemate.

Ignore the tactical feints. History says you cannot appease a dictator, who after years of power, has progressively discarded all limits, resulting in, “…absolute power corrupts absolutely.” Unfortunately, we are now seeing Putin’s mailed fist no longer hidden by his velvet glove. His mystical decision to invade Ukraine was for his own reasons, and had absolutely nothing to do with the real common challenges faced by his nation and the world in the very near future. This is a picture of a newly appeared Siberian sinkhole in the melting permafrost.

{kind=link}

1 These are somewhat remediable relative to the crucial major issue.

7/8/22 –

This is how we plan to invest our portfolio that is presently mostly in cash – in somewhat volatile bonds and in more volatile stocks. By the end of the year we should be totally invested 50/50, with the exception of some reserved cash. We strongly suggest that you consult with your qualified investment advisors about the following strategies:

Bonds

The reason for spreading our indexed bond investments out, likely on a monthly basis, is not to maximize returns, but to minimize the regret of being wrong in our timing. Bonds are a very crucial element in maintaining portfolio income, if you wish your portfolio to maintain itself over the long haul.

Stocks

Stocks are not the same as bonds. They are more volatile, having a longer duration (payback) period, and their long-term investment returns can now be measured in relation to long-term bond rates. What we are looking for, to justify a long-term investment in stocks, is an 1% spread of the S&P 500 over the long-term BAA bond rate. This will require a substantial further decrease in the stock market. When this spread is approximately reached, we will look to the markets for timing and will invest larger amounts than in the case of bonds.

We think this strategy makes sense for us. Both assets are capable of responding to technological change. There is just one further crucial point. We are necessarily treating the financial markets as if conditions will remain normal. But what On to be done about climate change after the next ten years and carbon emissions? If the political systems can deal constructively with climate change, the cost of capital will go up as more public works become necessary. If they can’t, then increasing chaos will ensue and real earnings will go down. This is a general observation.

If you are concerned with preparing the next generation for meaningful careers, you might ask what “meaningful” means if those running the political systems do not respond appropriately soon. At the end of Voltaire’s Candide, the hero having traveled in search of the best of all possible Enlightened worlds, came to the disillusioned conclusion that, “It is necessary to cultivate one’s (own) garden.” That is exactly what people can no longer do. It is really necessary to deal with the problem of climate change, to “Make haste slowly.”

7/27/22, 8/11/22, 8/19/22 Postings Restored.pdf – primarily about inflation and general financial planning.

9/22/22 -

On September 21, the Fed raised interest rates by ¾% to a level of 3 ¼%, still below the current rate of stubborn inflation. In August, the U.S. Personal Consumption Index (PCE) excluding food and energy rose by 4.6%, way above the long-term Fed target of 2% inflation. Inflation is getting entrenched into expectations; the Fed Open Market Committee remains “condition base,” and voted for this increase unanimously.

It is likely the Fed will increase interest rates until all treasury obligations have a positive yield in excess of then current inflation (have a positive real return). On 9/22 these were the current yields:

9/22/22 Current Yields

Fed Funds 3.25%

2 Year Treasury 4.11%

10 Year Treasury 3.70%

This implies that the Fed era of high interest rates will be longer and higher than previously assumed. There is a reason for this. The Bank for International Settlements is a central bank for the national central banks. In its 6/26/22 Annual Economic Report, it sets that is likely to be world-wide perceptions of what inflation is, and when it is propagated. *

This report sheds light on how inflation can arise and propagate from sector-specific price shocks, and of the relative roles of cyclical and structural forces.

“When inflation is low, economies have “significant self-stabilizing properties.” In other words, energy price spikes can be contained. “High inflation…induces changes in more structural features of wage formation, such as indexation and centralized wage bargaining, which help entrench the regime.” Considering U.S. inflation data between 1/65-12/85 (a period of high inflation), increased prices for food and gasoline were the major exporters of ‘spillovers’ to other economic sectors. In the future, we might note the increasing costs of food and energy, due to the stresses of climate change.

The best central bank policy is not to let general inflation even get started. “Transitioning back from a high-inflation regime can be costly once it becomes entrenched. All this puts premium on a timely and firm response. Central banks fully understand that the long-term benefits far outweigh ant short-term costs.” The central banks are likely to take heed of this. Inflation’s best economic effect is when it is negligible.

But it is a mistake to assume anyone can hit the top or the bottom of interest rates. We will probably increase our bond portfolio again within the next one or two months, because bond returns are much higher than previous.

*For those who are interested, this easy-to-understand report is also an excellent discussion of how general economic concepts affect specifics.

11/3/22 –

Third quarter earnings are out for VZ and NEM. Earnings are down

relative to the previous quarter and year due to the immediate impact of

inflation upon costs, and the delayed impact of inflation upon revenues. We do

not think they will have any problem maintaining their dividends over time

periods measured in many years. Due to the following, NEM has been dropping;

but the company has its costs under control and reports its finances

conservatively.

11/10/22 -

The October inflation report indicated a very slight moderation of the

core inflation rate, excluding food and energy, from a revised 6.6% in

September to a 6.3% October core rate. Conditioned to “buy the dips,“ traders

caused the ten year bond yield to decrease from 4.15% to around 3.92%, and the

S&P 500 to correspondingly increase. It is true that a recession, if any,

will be over within a year or two. Does this mean locking in higher long-term

rates right now; or will there be an upward shift in all financial market

yields due to both increasing Fed funds rates and increasing long-term

inflationary expectations? We expect the latter. That means that our next lock

point will likely be above the present intermediate bond ETF yield to maturity

of around 5.5%.

To stop inflation as soon as possible before it becomes further

embedded, the Fed has raised rates quickly. At a news conference after the Fed

announcement of a ¾ % rate increase, Chairman Jay Powell suggested that it was

premature to look forward to rate decreases. It is better to overtighten, using

available tools to support the economy; than to undertighten

and let inflation get away. Thus, the likely track of Fed policy towards high

interest rates will last longer.

Our portfolio is presently around 50% in cash; before increased

investing in long-duration assets – either stocks or bonds. * The financial

panic of 2008 had one originating cause, the housing crisis. Present

uncertainties: climate change **, deglobalization and that horrendous war in

Ukraine are multiple causes. The way for a value investor to handle these

uncertainties is, at least, not to overpay; to expect at least a positive risk

premium from stocks. We look for a long-term return of around 7% on the S&P

500. If this is not available in stocks, then we will invest in bonds to lock in

rates. It is also no fault to remain, for a while, in cash - which is finally

earning a decent rate of return.

* We would much prefer not to

get into wholesale market timing; but this is a substantial fact: if one had

avoided the excesses of very overvalued stock and bond markets; then one must

reinvest appropriately at a better price. We don’t think that always to be

fully invested is the correct thing to do; the alternative is to have to get

the markets approximately right, and to maybe suffer some further minor losses.

It would be better for all that markets not be overvalued relative to their

real business prospects. An analyst once said, “That company is irrational; its going to crash.” It did.

** To get a general idea of how much adaption to climate change will

cost; the International Renewable Energy Agency estimates by 2050 that the

total cost will be $131 trillion, on a per year basis about 5.5% of the world’s

2021 GDP. To limit a temperature rise to no more than 1.5 C![]() over the preindustrial level (if possible);

any reasonable target will have to be met by a combination of governments,

businesses and consumers, thus raising the cost of capital in the financial

markets over the long-term. The alternative of doing nothing will be even more

costly.

over the preindustrial level (if possible);

any reasonable target will have to be met by a combination of governments,

businesses and consumers, thus raising the cost of capital in the financial

markets over the long-term. The alternative of doing nothing will be even more

costly.

11/15/22 – revised

From Keynes onward, it has been noted although stocks are clearly very

long-term assets; with a payback duration of over 36 years, their pricing in

markets is very short-term. If portfolios are structured for the long-term,

then a longer-term view is necessary. That longer-term portfolio view,

particularly for those interested in other things, is inflation protected

income – stocks for long-run inflation protection. At a current rallied

11/10/22 S&P 500 price of 3956, its current dividend yield and equity risk

premium are clearly inadequate. To ask a question: do investors expect future

real dividend growth in the present international climate to be very large?

This may be formally shown by comparing the present value of stock returns with

current available bond returns:

Logical

Expectation 11/10/22 Actual

Market 11/10/22

2% Policy Rate

3.83%

2% 10 year treasury premium - 0.01%

2% BAA corporate bond premium

2.36%

1% Equity risk premium (S&P 500=3956) (-1.48%)

7%

4.70%

As can be seen from the above, the current BAA bond

YTM is 6.18%; but the present value of equity returns is only 4.70%. If you buy

BAA bonds, you can get a 6.18% return over around 7+ years. If you buy the

S&P 500 you can get a 4.70% return over 36+ years. As a long-term investor,

which would you choose?

Now to interest rates. We have just increased our

portfolio bond holdings to our target, around 50% intermediate term corporate

bonds. The total YTM of those bonds will be less than the BAA rate above, due

to our gradual phasing into this position and due to the ETF holding of

slightly lower-rate A bonds. But bonds at these higher rates haven’t been

available in ten years. We had originally hoped for a lower price than 75.5 and

certainly lower than the last price of 77.35. While we, obviously, remain very

cautious about the stock market, we are now at our bond target.

The reason for this is the latest October core CPI

reading of 6.3% (which we dismissed above) and the latest 11/15/22

October core producer price reading of 6.7% on an annual basis, and unchanged

in October. This signals that the momentum of inflation may have been broken

(except for international developments) and that the Fed’s job of decreasing

inflation to the 2% level may be slightly easier. The producer price index

leaves out increasing real estate rentals (but factors in construction costs),

the cost of imported goods and domestic distribution costs. It differs from the

CPI due to its perspective at the producer rather than the consumer level. The

economists, who expected a decrease of inflation due to the moderation of input

prices, may be right…in the very long-term. The Fed still has difficulties

decreasing inflation, but their job will be somewhat easier due to the

subtraction of momentum. This means, ultimately, a highly inverted bond yield

curve with a lessened risk of further long-term bond price depreciation.

Investing is

not, however, without risk; that’s why risk premia exist. If Europe has a cold

winter, the cost of energy and long-term bond yields will spike again. But we

are now taking much less risk by increasing bonds than stocks.

12/07/22

–

We have

locked in a long-term bond return of around 5.25% for around 50% of our

portfolio. The .25% lower return than target is due to the fact that we chose

to minimize risk by spacing out bond increments over months. Furthermore, the

consistently accurate prediction of interest rates is impossible even for

professional bond traders; we are generally satisfied with this bond lock-in.

In addition,

in December, bond ETFs and mutual funds distribute their realized losses and

gains for the year to their shareholders. This year, we expect a meaningful tax

benefit for those bond losses realized before we had invested, this advantage

accruing only to currently taxable investors.

Now, about

the lock-in of the equity proportion of our portfolio. We invested around 16%

of our portfolio in two stocks, for their dividends, which we will continue to

hold. We will later discuss why we invested in these stocks about a year ago,

and the lessons learned.

A value

investor is very concerned with the initial investment price, the future value

that one gets for the present money. As the saying goes, “A stock doesn’t know

you own it (but you do).” Many investment people will say that its always a good time to invest. That may make business

sense; but it doesn’t necessarily make client sense. A high market valuation

precludes further investment around 10% of the time.

We have

calculated an annual long-term rate of return on the S&P 500, a diversified

portfolio of stocks. This rate of return is not particular to us; but is

generally true. A New York bank investment department exactly follows our

analysis of S&P 500 returns.

Our analysis 7/2/21: BAA bond rate = 3.3%; S&P 500 level =

4352; 10 yr. avg. operating EPS=125.33

Calculated Annual Return of the

S&P 500 = (125.33/4352) X 1.33 =3.83%

60/40 Portfolio Return

S&P 500 = 3.8% x.60 = 2.3%

BAA bond rate = 3.3% x .40 = 1.3%

Annual Portfolio Return 3.6%

Excerpt from the 7/21 NY

bank report, p.3: “However, our

forward-looking portfolio returns do not come close, at 3.6% for a U.S.

60/40 vs. an inflation rate of 2% annualized over the next 10-15 years.”

The stock market has been badly overpriced in the last few years due to abnormally low interest rates. With the return of the bond market to more reasonable levels, our major concern is now when to lock in equity returns for the remainder of the portfolio. As we said, we don’t much like market timing; but we really have no choice. The financial markets have been overvalued for years.

Due to the Ukraine war, deglobalization with supply chains closer to home and climate change we think the economy will be increasingly supply constrained. This will raise the cost of capital, and thus it makes sense, at least, not to overpay for stocks. A 2707 level of the S&P 500 will presently result in a 7% long-term rate of return on capital; considering markets, we would add “approximately.”

What have we learned from this year? We found out that in a normal economic environment, value investing in individual stocks makes a lot of sense. The effect of losses on our portfolio have been minor; but could we have done better? The answer is, yes but. At the end of last year, we had invested in VZ and NEM, expecting but a slow increase in inflation (it had been very low in the last decade). What, in fact, happened was a rapid rise in inflation and a countering rapid rise in short-term interest rates, resulting in an immediate effect on company expenses, but not on revenues.

Financial Times; 11/30/22

The basic problem here is not that we overpaid for the long-run, but invested at close to the stocks’ “fair” or equilibrium prices. In fact, we could have waited another year until the prices dropped another 20% or so, making both value stocks. Could we have invested less in these stocks? The answer is, of course; but the income effect on effectively a 0% portfolio would have been much less. Our portfolio is configured for long-term income, rather than for short-term capital gains. Some lessons the market teaches are worth heeding *; many are not because often a short-term lesson learned turns out to be the right thing to do because the entire financial regime has changed. Therefore markets are so fascinating.

Looking forward:

Having substantially avoided a very expensive adventure into media, in 2021, Verizon spent $47.6 billion purchasing additional spectrum bands from the government mostly in the valuable C band, ranging in mid frequency from 3.3-4.2 GHz. Verizon was the winning bidder of 3,511 licenses in all 406 markets available in that auction. This C band is supposed to be the “ultimate sweet spot” which blends speed, range, penetration and capacity. This is likely to be a good use of company capital. But the large Verizon network is presently configured to maximize utilization rather than to maximize speed, as competitor AT&T’s is. This has short-term marketing implications for both companies, because AT&T has some 5G advantage, using less Dynamic Spectrum Sharing than Verizon. That will likely change with 5G on the C band, which will eventually enable Verizon to dedicate the 5G network only to 5G services.

With the collapse of crypto, NEM has gained as central banks (Bloomberg, 6/8/22) and individuals seek to cope with uncertainty, buying gold. The problem with crypto is that it is all increasingly high energy expense (as various sites compete to add a new block of transactions to the blockchain), possessing no positive intrinsic value. National fiat currencies are, in theory, backed by tax revenues.

Although these two stocks are long-term investments, we would keep a general attention over time. In specific, also, VZ and NM should begin to improve their operating margins; VZ next year. add: If we were to further simplify our portfolio, we would wait until these two stocks reached historical cost; and then simply buy the S&P 500 index with the proceeds, to round out the rest of the portfolio.

* One lesson that is really worth heeding: To make decisions on individual stocks, people should first decide whether, by nature, they are value or growth investors. Value investors look for bargains (when growth investors give up) and growth investors during up market phases (leave value investors behind). In the ecology of functioning markets, both are necessary to complete the buy and sell sides of a transaction, value investors setting the floor and growth investors moving prices upwards.

Professor Amar Bhide of the Fletcher School sums up the difference between value and growth investors in markets: “The dynamism of our economy also requires both sensibilities. In Max Weber’s classic formulation, thrift is the bedrock of capitalism while Deidre McCloskey includes bourgeois prudence. And thrifty prudence which disdains, this time it’s different rationalization, promotes the efficient exploitation of existing resources, releasing more capital for more investments. (Our background is bank credit.) But capitalist economies would not survive just by investing in more of the same. Their adaptability, technological progress, and appeal to the human love of adventure, requires innovators whose dreams defy objective calculation of the risks and returns and investors with the guts to back them.”

And also: There is room in many portfolios for investments, no more than 10% of the total stock portfolio, that are illogical by the first paragraph. We have one close to venture capital investment (less than 1% of the total portfolio) in a self-driving truck company, run by the former head of Google’s self-driving car subsidiary. The company has industrial partnerships with many truck manufacturers and has a strategy of beginning by running simple truck routes across Texas. They seem to have a good chance at success, we hope. Your portfolio should also be a source of enjoyment; its a chance to really learn about investing and your investments.

__

A 12/09/22 FT article states the usefulness of having a certain financial management philosophy:

“Being financially resilient, slowly building your investments (not aiming to win the lottery) and retiring more comfortably by the age of 70 may not be meme-worthy, but these are the messages that should have far greater influence.”

1/12/23 –

The important CPI release

of December, 2022 shows that the Fed’s policy of higher interest rates is

beginning to take its effect on the economy. For the last three months of 2022,

consumer costs of all items, less volatile food and energy, increased at an

annualized rate of 3.2% - compared with the June-Sept annualized 6%. Consumers

costs of services, less energy, increased at an annualized rate of 5.6% -

compared with the June-Sept annualized 7.2%. The prices of consumer goods and

services have decreased meaningfully in the last three months, but both are

still quite far from the Fed target of

2% annual inflation, where that level should have no effect upon the

allocation of economic resources.

Although inflation

originally started in the goods producing sectors, it has now spread to and can

sustain itself by increasing labor costs. The Fed, now able to control

inflation with smaller future rate hikes, will likely maintain a regime of

monetary restriction for longer to control these costs.

If this is so, U.S. equity

remains very overpriced relative to its 36+ year payback period. Also, the

looming House Republican effort to roll back Social Security, Medicare and

possibly taxes; by refusing to raise the U.S. debt ceiling, will cause a lot of

problems.

Logical Expectation 1/12/23 Actual

Market 1/12/23

2% Policy

Rate

4.33%

2% 10

year treasury premium - 0.90%

2% BAA corporate bond premium 1.97%

1% Equity risk premium (S&P 500=3983) (-.64%)

7%

4.76%

In these analyses, we have

been making one crucial assumption; that the far future will be like the past.

Most crucially, the present value of stocks includes 2% real growth and 2%

inflation; and that a 4% annual spending rate from a well-bought financial

portfolio will enable it to last a very long time. Climate scientists now say

that mankind is proceeding from the recent Holocene era, when Mother Nature

kept things relatively stable thus enabling civilization in the last ten

thousand years, to the Anthropocene era where we determine our own destinies.

Will the far future be like the past? As those who have lived through a few

historical events can testify, it never is. But can the far future be somewhat

like the past? We hope so; for the stability of human arrangements and

institutions depends on that. We shall discuss this in our next essay.

3/4/23 –

Amid the clutter, one fact

is beginning to stand out. As one noted economist succinctly said, “Inflation

isn’t going anywhere.” Using data to Jan-Feb 2023, the following Financial

Times graph illustrates this:

Due to the COVID epidemic

and years of world-wide monetary expansion, inflation is a problem.

We had originally hoped

that, with some alacrity, U.S. equity returns would have gotten in line with

bond returns. But, as our following analysis illustrates, this has been not the

case:

Logical Expectation 1/12/23 Actual Market 3/2/23

2% Policy

Rate

4.57%

2% 10

year treasury premium - 0.49%

2% BAA corporate bond premium 1.82%

1% Equity risk premium (S&P 500=3981) (-1.14%)

7% 4.76%

The above suggest

something about human behavior in financial markets. Conventional financial

economics assumes a uniform behavior in markets, according to some universally

held statistical model. But that is not the short-term behavior of auction

markets, where participants have but to consider three things: the bid, the

offer and their willingness to do the deal. To consider the future, a present

value model and a likely rate of investment return is necessary to make the

stock investment comparable to bonds, and that return must include the effect

of inflation. Thus the above.

In a previous essay, The Nature of Stock Market Equilibrium,

we noted that among the financial variables we considered, inflation was the

least well-behaved, i.e. it was not placidly Gaussian (as the others were at

the time).

To control the effects of

inflation, resulting from the changing of the economy from insufficient demand

to insufficient supply; now there is too much M2 (primarily cash, checking

accounts and CDs); monetary policy has to become restrictive. But no easy

adjustments along an unchanging Philips curve. A rule of thumb is that a

restrictive Fed policy rate should be above the rate of inflation. This is

presently not the case, with Fed Funds currently at 4.50%-4.75% and US core

inflation at 5.6% for the month ending January, compared against the previous

12 months. A 3/3/23 Bloomberg analysis by Larry Summers of Harvard and a

former treasury secretary, notes: “…six recent jolts have hurt the possibility

of a soft landing that the Fed has sought…

·

Seasonal

revisions to the consumer price index that (have resulted in taking) the

downward trend of inflation out of the data for the last several months of

2022.

·

The CPI for

January showed an acceleration of inflation.

·

The personal

consumption expenditures price index also picked up.

·

January economic

indicators ‘read strong.’

·

Wage figures ‘no

longer show the kind of reductions that we had been expecting.’

·

The jump in

Treasury yields, with 10-year rates climbing past 4%.”

Our portfolio goal of 50%

equities is going to be deferred, and holding some cash isn’t a bad idea.

__

U.S. CPI data of 3/14/23

reveals that the core rate of inflation, excluding food and energy, remains

stuck at a very high level. Compared with a 5.6% rate in January, core

inflation in February decreased to only 5.5%. Inflation remains high; but

Silicon Valley Bank collapsed - there are problems. Consider the fate of SVB,

which bet on lower interest rates; does an investor want to increase the

duration of one’s portfolio at this time.

3/31/23 –

On the above date, the

S&P 500 closed at 4109, yielding a long-term investor a rate of return of

only 4.66%. Although there has been some

rally in the bond market, a large 7% YTD rally in the stock market has reduced

the S&P 500 return to more unacceptable levels. Its moments like these that

reveal the truth; are you a value investor or a momentum investor? Essential

contradictions are not good in the long-run.

Logical Expectation 3/30/23 Actual

Market 3/30/23

2% Policy

Rate

4.83%

2% 10

year treasury premium - 1.28%

2% BAA corporate bond premium 2.11%

1% Equity risk premium (S&P 500=4109) (-1.00%)

7%

4.66%

Another

measure of the S&P500’s valuation is its price/sales ratio, which still

exceeds the level reached during the dotcom boom of 2000.

{kind=link}

This posting

will discuss our portfolio policy. How can we get rid of essential

contradictions? Maybe ChatGPT- 4 can help. Give it a

problem that contains an essential contradiction: What happens when an

irresistible object hits an immovable wall? Its answer is impressive, true, but

not useful in a complicated real-life situation. Here is the answer: “The

scenario described cannot happen in reality. It is a classic example of

a logical paradox, where the conditions set up in the question are

self-contradictory and cannot be resolved.”

So what’s

the solution between two contrasting investment philosophies, value investing

(value) and modern portfolio theory (optimal diversification)? The answer is

logical subordination. To meet future conditions, approximate portfolio

asset diversification is very necessary. At the same time, an investment in the

automatically diversified S&P 500, at the right price and therefore

rate of return, is also desirable.

Here is why.

Richard Bookstaber has a PhD in economics from MIT,

after a career in risk management on Wall Street, he was the Chief Risk Officer

at the University of California, managing its $180 billion investment

portfolio. In a 3/27/23 NYT article titled, “The Slow Motion Tidal Wave

Consuming Our Economy,” he wrote:

“Our economy today has been described variously as “weird,”…Weird because this is a yo-yo economy where gas prices shot up to more than $5 a gallon and then settled back down…Housing has gone from boom to bust, then to boom again….There’s a weirdness yet to come, and a lot more than run-of-the-mill weirdness. We are entering a new epoch of crises, a slow-motion tidal wave of risks that will wash over our economy in the next decades – namely climate change, demographics, deglobalization and artificial intelligence. Their effects will range somewhere between economic regime shift (see what happened to our first stock market model) and existential threat to civilization. The risks to the economy, to the stability of our society and to civilization are enormous if we don’t get the economic models right for what’s coming.

“For climate, we are seeing a glimpse of what is to come: drought, floods and far more extreme storms than in the recent past. We saw some of the implication over the past year, with supply chain broken because rivers were too dry for shipping and hydroelectric and nuclear power impaired….We are reversing the globalization of the past 40 years with the links in our geopolitical and economic network fraying….The geopolitical forces behind deglobalization will amplify the stresses from climate change and demographics to lead to a frenzied competition for resources and consumers….

“The problem

here is not that our economic models don’t work at all. The models seem

serviceable when things are simple and stable, when we are in a steady state

with tons of data to draw on. The problem is that the models don’t work when

our economy is weird….

“A key

reason these models fail in times of crisis is that they can’t deal with a

world filled with complexity or with surprising twists and turns.”

Bond

investors tend to be more conservative than stock investors because their

returns are fixed by contract. What they are talking about now is

“optionality,” to have the flexibility within a portfolio to handle new events.

Professional bond investors can achieve this by buying complicated options and

contracts. Most investors can achieve some of the same result by holding more

cash than is usual. In contravention of a 50/50 split formula, this is what we

will likely do because there is the possibility that the cost of capital will

increase in the future due, to repeat, due to 1) climate change 2)

deglobalization 3) a decreasing work force. All these have the potential to add

to inflation, and an increase in interest rates. Our intermediate term bond

portfolio has a duration of 6.2 years, the S&P 500 portfolio bought at

equilibrium (just guessing) probably has a duration

* of 21 years, and cash has a 0 duration. If interest rates increase, then a

portfolio holding 10-15% in cash will have a total duration around 12.2-11.6

years, and a possible like percentage decrease in value for every percentage

point increase in long-term interest rates.

Since the

resulting portfolio will probably have an interest sensitivity of

12.2-11.6%/each long-term percentage change in rates, in an era of likely

increases, we are 1) not going to overpay for equities beyond an approximate

target rate of a 7% return and 2) will hold a minimum cash of 10% to 15% in our

portfolio. 10% is likely for us because we have gone through all that trouble

to calculate the rate of return of the S&P 500. But we hope the future will

be somewhat like the past; and that is the role of effective government meeting

new circumstances. Hunter-gatherer societies tend to go extinct when the

environment changes.

What we have

done is to add optionality to the traditional portfolio tradeoffs between risk

and return.

* Third icon

for the article. Silicon Valley Bank should have read this. A bank usually

lives with the fear of God, fearing a run on the bank. But, in this justified

instance, an effective government guarantee of depositors creates an incentive

to treat investments, with Other People’s Money, with less care because now

what is at risk is only the capital of the bank and not that of its depositors.

SVB took a gamble that the level of interest rates would stay low, also

enduring a duration mismatch between its assets and the liabilities of its

volatile depositor base. The antidote has to be more stringent regulatory

supervision for banks like this, still maintaining some uncertainty about who

will be responsible for the assistance should trouble occur, to avoid public

pressure and moral hazard (Kindleberger, 2011 ed.).

__

The

determination of future interest rates all involves estimates What central

bankers approximately look for is R*, the real neutral rate, the short-term

interest rate what would prevail in the economy at full employment absent

stable inflation. According to a 4/10/23

Bloomberg article, a .5% International Monetary Fund R* assumption, with 2%

inflation, would predict a policy rate around 2.5% - driven by aging

populations and sluggish productivity. Economist Larry Summers predicts the Fed

policy rate, rev. which includes inflation, to be slightly less than 2% + 2% because of stepped up military outlays and

transition to a greener economy. Using reasonable markups to equity, the IMF equity

assumption would be around 7.5%; and the Summers assumption would around 9%.

(Remember the era of 8% corporate bonds?) Applied to equity, the Summers

assumption is certainly historically, if not currently, reasonable.

So is the

lock point around a 7% equity return or a 9% one? Choose. The current level of

the S&P 500 is 4109. A 7% equity return would be a level of 2735, not

unfeasible in the current environment. A 9% equity return would be a

level of 2127. We tend to be around the 7% level with some optionality; and by

the way, note the 2% constant inflation assumption – where we also assume there

can be a tradeoff between real returns and inflation.

This is what

we will likely do. In finance, there are three choices:

1)

Make

a decision and be either right or wrong.

2)

Speak

out of both sides of your mouth. (The usual strategy.)

3)

Make

a decision and recognize that there is an optionality cost.

In stock

market investing, which is inherently uncertain but not random *, we prefer the

third.

*Actually,

we could say a lot more about that; but we won’t in the interest of brevity.

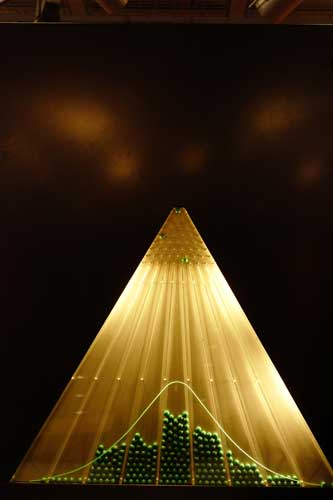

But the Galton Board models the

behavior of an asset in MPT. The problem is that in financial markets the news

doesn’t arrive in discrete random chunks. Particularly regarding climate change

or defense expenditures, the news is very much serially correlated, like a real

story; and moreover people in markets have different interpretations and credibilities. Stories, by the way, are how people handle

complexities. So, get the general narrative right about the future.

{kind=link}

We promise

we won’t belabor this further. We asked ChatGPT why

the Galton Board has a last row of horizontal pegs. Is this cheating? ChatGPT-4

(at this time) seems not to handle specific details too well. Answer:

“The last row of horizontal pegs in a Galton board allows the balls to be

evenly distributed across the bottom of the board before they are

collected in bins. Without the last row of pegs, the balls would all land in

the same area…” The Galton Board, however, is supposed to produce a normal

distribution because the top of the funnel is smack in the center of the other

pins. It should therefore determine the most probable subsequent path, which is

the median or average of a Gaussian distribution.

Maybe the

point of the horizontal pegs (in this specific configuration of the Galton

board) is to pre-sort and slow down the balls, so they will land in their

proper bins. That’s probably it.

__

We have not given

a definite, or most probable, prediction. Here is the reason why, specific to

this time. We have been discussing how stock market returns are dependent on

the future natural, economic and social environment. At this time, the future

of this environment is not clearly obvious, being highly dependent on the

decisions on what we and government make in the next few years. To preserve

capital, we do however assume that the future will be somewhat like the past

(but surely not perfectly).

Mohamed El-Erian is the President of Queens’ College, Cambridge and

former CEO of PIMCO, the major bond investing firm. In his most recent book on

central banks (2020), he writes:

“In explaining what lies

ahead and why, my strong preference would have been to do so by asserting a

single high-probability base-line. Such an approach provides clarity,

assertiveness, and confidence as to outcomes. It avoids the dangers and

accusations of appearing wishy-washy and indecisive. And, as a friend joked

with me, it is much better to sell books! Yet as attractive as such an approach

is, it is simply not a feasible option given present realities. Indeed, it

would also be intellectually dishonest and analytically irresponsible to do so

in the times in which we live.

There is simply too much

fluidity in each of the four major factors that currently impact much of our

collective well being (economic…political…market…and

policy…), and the intersection of the four – which is where the real world

operates – is even more fluid (when combined).

As such, it is important, if not paramount, to think more broadly,

including breaking away from the usual confines of well-behaved (gaussian)

bell-shaped distributions that have the comforting attributes of very high

expected outcomes and thin tails. We need to be able to embrace the increasing

possibility of…more extreme outcomes, both good and bad. * Adding to the

complexity, the journey is far from predestined…”

We have been talking about

the behavior of financial assets in markets. Remember a saying, “Keep some

powder dry.” We hope that the financial

economy will remain in substance, but must also consider increasing real

changes in the environment and in the economy – and government’s appropriate

response to these, which voters should consider and require.

* Such as occurs when

there is a change in financial regime, from requiring Keynesian demand

management to requiring the management of supplies. The latter requires a

political consensus about the direction of a society.

__

There are also present problems.

According to the NYT (4/27-28,2023):

“Two years ago, high

inflation was about supply shortages and pricier goods. Then it was about war

in Ukraine and energy. These days, services are key….America is now two years

into abnormally high inflation – and while the nation appears to be past the

worst phase of the biggest spike in price increases in half a century, the road

back to normal is a long and uncertain one….

“(in the month of

March)...after stripping out food and fuel prices, a closely watched “core”

index (of the PCE) held nearly steady last month That measure rose by 4.6

percent over the year, compared with 4.7 percent in the previous (February)

reading…”

The Fed long-term goal for

PCE inflation is 2%. There is a way to go, and that process will affect either

inflation (ultimately interest rates) or the real economy (the trend in

earnings). Thus we maintain a substantial position in cash, and don’t mind

“missing out.”

6/04/23 -

We sat in on a MBA class

at a noted business school. The case under discussion was a fast-growing

company that had financed long-term building lease payments (liabilities) with

the short-term tenant leases (assets) – the mirror image of Silicon Valley

Bank. A comment: “That company is illogical; its

going to crash.” The company’s stock price subsequently cratered.

The U.S. has narrowly

averted default on its obligations. To mention a similar illogicality in the

finances of the United States. The U.S. wants a social welfare system (no cuts

in social security and medicare) but doesn’t want to

pay for it with additional taxes (due to a legacy going back to the Revolution

of 1776). The gap between government expenses (made worse by COVID) and

revenues (taxes) has been made up by having foreigners finance the resulting

U.S. deficit.

From OECD data, total

U.S. government revenues; federal, state, and local; as a % of GDP are

comparatively very low.

All Government 2020 Revenues As a

% GDP

United States 25.8

Australia 28.5

United Kingdom 32.1

Germany 37.9

Sweden 42.3

Denmark 47.1

The following illustrates

the U.S. budget deficit, which in Feb 2023 is projected to increase due to net

interest outlays (even assuming a moderation of inflation) and increasing

social expenditures.

To discuss inflation: A

business economist recently said, succinctly, “Inflation isn’t going anywhere.”

This CBO projection of core inflation a/o Feb 2023 expects a rapid decrease in

the period 2022-2024 as the price of goods drop. Due to previous monetary

creation and continued robust economic growth that may not happen. Inflation

also makes this situation unsustainable in the medium-term; these deficits will

become increasingly difficult to finance, as the U.S. turns to foreigners (i.e.

high-savings countries), to buy its debt. The adverse effects of excess

inflation (above 2%) upon interest rates, the cost of capital, should be

obvious.

The U.S.

cannot have both low taxes and social programs.

__

In first

quarter 2023, Verizon improved its cash flow dividend coverage after scheduled

capital expenditures. But the company has problems in marketing and profit

growth. Verizon has recently simplified its consumer offerings, giving its

customers choices of Disney+, Apple TV ; also International Travel Pass and Walmart

delivery. These content offerings make sense for the nation’s largest network.

06/29/23

–

At the end of 2021,

the financial markets assumed that interest rates would not increase much

because inflation was absent. Inflation subsequently increased. In 2023, the

financial markets assume that inflation will shortly return to the 2% level.

The S&P 500 has

rallied under the assumption that interest rates would drop. The exhibit below

illustrates this, but the decrease in inflation has been very slow. In May, the

consumer core PCE slowly decreased from 4.7% to 4.6%.

Long-Term Logical Expectation

Actual Market 6/26/23

2% Policy Rate

5.07%

2% 10 year treasury premium

- 1.33%

2% BAA corporate bond premium

1.96%

1% Equity risk premium (S&P 500=4342)

-1.29% *

7%

4.41%

* Assumes 2nd quarter

2023 high in CAPE earnings = average $144

The financial markets

are likely too optimistic, expecting a rapid return of an era of 2% inflation

and 2% policy rates.

The current stock market

level of 4342 says that the economy, on the next 12 month S&P earnings

estimates of $229, will have a return of exactly 7% if the stock market never,

ever has an earnings downturn (sounds typical, subsequent growth occurring

at 2% real and 2% inflation in perpetuity). This in spite of Fed efforts to

combat high inflation, changes in demographics, the effects of global warming,

international events, and the need to transform the U.S. economy – all of which

should increase ke , the cost of equity

capital or the rate of required return by investors. We would not head for the

stock market.

__

In 1949 Benjamin Graham

wrote, “The Intelligent Investor;” “The best book about investing ever

written,” as Warren Buffet said. He wrote, “Imagine that in some private

business you own a small share that cost you $1,000. One of your partners,

named Mr. Market, is very obliging indeed. Every day he tells you what he

thinks your interest is worth and furthermore offers either to buy you out or

to sell you an additional interest on that basis. Sometimes his idea of value

appears plausible and justified by business developments and prospects as you

know them. Often, on the other hand, Mr. Market lets his enthusiasm or his

fears run away with him, and the value he proposes seems to you a little short

of silly.”

Five large tech

companies have accounted for more than 80% of the S&P500 ’s 2023

appreciation. The rest of the S&P 500 being somewhat cyclical, can people

count on these five companies to never have an earnings downturn? That is what

the stock market presently assumes. Nifty fifty again?

__

We invest according to

the business fundamentals: that is according to what a company supplies to the

economy and how profitable that may be in the future. Relevant to portfolio

returns are interest rates and a desired rate of equity return, we can then

price equities to their fundamentals. Why invest according to those

fundamentals, when the behavior of markets is sometimes interesting? Because,

in the long-run economic fundamentals, as we shall give an example of,

dominate. Serious investors should consider the fundamentals.

First, some quotes

from two accomplished value investors, J.M. Keynes and Benjamin Graham:

Keynes: “But there is one feature in particular which

deserves our attention. It might have been supposed that competition between

expert professionals, possessing judgment and knowledge beyond that of the

average private investor, would correct the vagaries of the ignorant individual

left to himself. It happens, however, that the energies and skill of the

professional investor and speculator are mainly occupied otherwise. For most of

these persons are, in fact, largely concentrated not with making superior

long-term forecasts of the probable yield of an investment over its whole life,

but with foreseeing changes in the conventional basis of valuation a short time

ahead of the general public. They are concerned, not with what an investment is

really worth to a man who buys it ‘for keeps’, but with what the market will

value it at, under the influence of mass psychology, three months or a year

hence.” The General Theory, chapter on Long-Term Expectation. Provided

an investment is properly chosen according to its fundamentals, individuals

have the great advantage of time.

Graham: “…our book is not addressed to speculators, it is not

meant for those who trade in the market. Most of these people are guided by

charts or other largely mechanical means of determining the right moments to

buy and sell. The one principle that applies to nearly all these so-called

‘technical approaches’ is that one should buy because a stock or market has

gone up and one should sell because it has declines. This is the exact opposite

of sound business sense everywhere else, and it is most unlikely that it can

lead to lasting success in Wall Street. In our own stock-market experience and

observation extending over 50 years, we have not known a single person who has

consistently or lasting made money by thus ‘following the market’ (our note:

because as the market increases in price, its long-term rate of return goes

down).” The Intelligent Investor. We really recommend this book, which

states the core of value investing – some form of fundamental value

determination; and then for individual stocks, a margin of safety.

A quick test for

reasonableness: The duration (payback

period) of the S&P 500 is presently probably around 20+. years. To get to a

previous generation of prices, before COVID and before the financial system

meltdown of 2008-2009, we analyze the rate of return available for the S&P

500 on 6/30/03. This would have been a time of millennial free market

enthusiasm. We just chose the date, somewhat at random, without first looking

at the result.

S&P 500 (Shiller)

CAPE earnings 6/30/03 = $43.05.

Investor Required Rate

of Return= 10 yr. treasury + 3% (to account for corporate and equity

illiquidity risk)

= 3.54% + 3% = 6.54%

S&P 500 calculated

level 6/30/03 = ($43.05/.0654) x1.33 = 875

Level S&P 500

6/30/03 = 974

3/31/03 = 848

12/31/02 = 879

7/25/23 –

Verizon has

technically the best network in the industry and due to a large expenditure on

broadband licenses, has the best possibilities for the future. But Verizon’s

consumer marketing has been of concern, because a continuing trend of slightly

decreasing earnings would eventually have an adverse impact on dividend

coverage. Second quarter 2023 company results indicate that the company is

starting to get traction with a simplified marketing plan to consumers and is

starting to decrease postpaid wireless losses. The company’s business additions

are also making a positive contribution. Through improved marketing, the

company is starting to get a lot more customer focused.

(Thousands of Lines) 1st Q 2023 2nd Q 2023

Consumer Wireless -263 -136

Business Wireless 136 144

-127 8

At the same time, the

company’s 2nd quarter reported cash flow decreased; but the cash

flow would have increased if the company had not incurred pre-tax $237 million

in employment severance charges and $155 million in asset rationalization chargeoffs, both adding to post-tax cash flow of around

$305 million.

Cash

Flow

(millions of

dollars)

1st Q

2023 2nd Q 2023

Net Income 5,018 4,766

Depreciation 4,318 4,359

Scheduled CAPEX * -4,688 -4,688

Available

for Dividends 4,648 4,437

Dividends

2,744 2,743

Coverage

1.69X 1.61X

* CAPEX approximately Depreciation

The company is

confident that it will maintain the growth in its yearly wireless service

revenue of 2.5 to 4.5 percent and maintain a 2023 EPS of $4.55 and $4.85. We

think that it can easily cover a dividend of $2.61/share.

Verizon is taking the

problem of lead sheathing in its copper network seriously. It does not believe

this is a very large problem with its legacy Bell network,

and is looking into its acquisitions.

8/8/23 –

The increasing cost of

capital has turned up in the increased return of the 10 year treasury bond, but

it has not turned up (yet) in the long-term return of the S&P 500, which

continues to decrease.

Long-Term

Logical Expectation Market 6/26/23 Actual Market 8/7/23

2% Policy Rate 5.07% 5.33%

2% 10 year

treasury premium

- 1.33% -1.24%

2% BAA corporate bond premium

1.96% 1.90%

1% Equity

risk premium (S&P 500=4342) -1.29% * -1.76% * (S&P

500=4518)

7%

4.41% 4.23 %

* Assumes 2nd quarter 2023 high

in CAPE earnings = average $144.

In the short-term

future are world-wide food problems caused by Russia’s continued invasion of

Ukraine, the continued residue of wage inflation, and a need for increased

supply chain security. In the long-term future are the capital demands to

combat global heating and adverse demographics. We do not think a 7% long-term

return is unreasonable. An optimistic assumptions level of the S&P 500, of

around 2740, is way below its current level. In the meantime, patience is not a

bad idea.

__

Equity markets go up

because earnings go up or the cost of capital (the rate of long-term return)

goes down. Equity markets go down because earnings go down or because the cost

of capital rises. But from the standpoint of investors, what ultimately carries

a portfolio, and its owner, through is real inflation-adjusted income.

Less volatile

intermediate term bonds provide a current income, which investors can either

save or spend. Then an emphasis either on a properly priced S&P 500 index

fund for inflation protection or on individual growth stocks depends upon what

a portfolio owner decides, on whether to spend time on stocks.

The thrill of the

chase, admittedly not an unimportant factor, should not be the dominant reason

to invest in a stock.